The Public Accounts Committee (PAC) report warns that there could be “potential disruption” at the UK border if cross-border passenger volumes, which have been at a fraction of normal levels due to the pandemic, recover as expected in 2022.

This could be “exacerbated by further checks at ports as part of the EU’s new Entry and Exit system and especially at ports like Dover where EU officials carry out border checks on the UK side,” the PAC’s report says.

“The PAC has repeatedly raised concerns about the impact of changes to trading arrangements on businesses of all sizes and we remain concerned.”

Since the end of the agreed transition period on 31 December 2020, there have been a series of changes in how the UK trades with the EU, and in relation to the movement of goods between the UK and Northern Ireland.

This has led to the EU introducing full import controls. While the UK had initially intended to follow suit, the implementation of such controls has been delayed by the government three times over the past year.

“Government plans to create the most effective border in the world by 2025 is a noteworthy ambition but it is optimistic, given where things stand today,” The PAC says, moving on to comment that it is “not convinced that it’s underpinned by the plan to deliver it.”

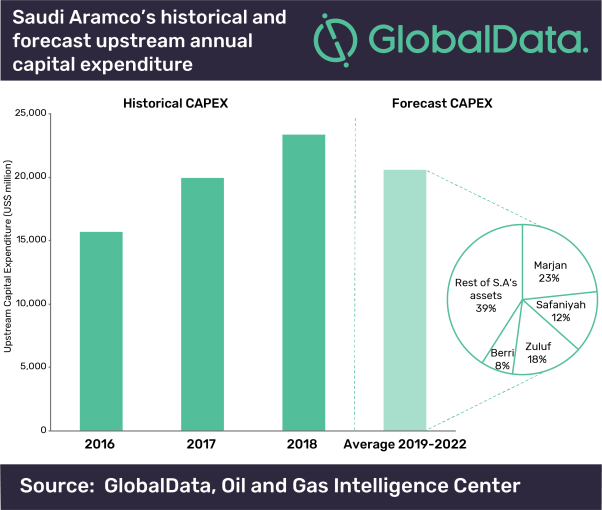

The company’s report, ‘Saudi Aramco After IPO – Company Overview and Development Outlook’, reveals that five major expansion projects – four crude and one natural gas – are being planned to boost output in the country.

One eighth of the world’s crude oil from 2016 to 2018 was produced by Saudi Aramco. As well as being the world’s largest oil producing company, it is also the most reliant on oil production, with 88% of its total 2018 upstream production coming from crude.

Somayeh Davodi, Oil and Gas Analyst at GlobalData, commented: “The major expansions at Saudi Aramco’s offshore oil fields of Marjan, Zuluf, Safaniyah and Berri are expected to comprise the majority of the company’s upstream investment over the next three years. Although these developments will also add gas and NGL capacity, the main addition will be oil.”

In 2018, the company’s MSC capacity (maximum barrels of crude oil that can be produced during a year) was 12 million barrels per day (bd) with 10.5 million bd oil produced plus the remaining 1.5 million bd available as spare capacity. This capacity allows flexibility to respond to market supply and demand fluctuations. The new expansions will add 1.45 million bd additional oil capacity.

Davodi adds: “Future production, including the ability to realize output gains from new capacity additions, is likely to be highly dependent on OPEC quotas. Production cuts are set to continue into 2020, but could be extended further.”

The only exception is errors, as they can be disputed immediately and removed. However, there are ways to address the other negative entries in your record. In this article, we’re going to show you the steps you should take to remove bad entries from your credit report.

Pull Your Credit Report

The first thing to do is pull your credit report to see if there is anything there. Just because an account has been in collections for a while and you’ve been getting calls and letters, don’t automatically assume that it was reported. If you are past due on an account but it hasn’t been reported to credit reports, you can still prevent the negative reporting by working with the company to pay the bill.

Businesslinkuae is the Best Business Consultancy for free zone company formation in Dubai, Setting up a business in Dubai is not a big deal now with Businesslinkuae.

Companies like Verizon, for instance, will often be open to dealing with you and finding a deal. If you want to know how to do that, Crediful has a few tips on how to handle past due accounts with Verizon and what you can do if it was already reported.

Know that it is not in their interest to send your account to a debt collection agency. Why? Because they aren’t actually collecting the debt on behalf of the company. Your debt is sold to them for pennies on the dollar, and they then accept the responsibility for your debt. Companies like Verizon would much rather strike a deal with you than lose their money. So if it hasn’t been long, chances are you can work out something before you have to deal with a bad entry.

Clean Up the Errors

A surprising number of credit reports have errors on them, and some of these errors do hurt your credit score. This is why you want to address all errors immediately and always make sure that you order your mandatory free copies from all three major bureaus - Experian, Equifax, and Trans Union - once a year.

For example, debts falsely attributed to you that belong to someone else or accounts that should have aged off your account should be removed. Debts might be duplicated or the amount is incorrect. There are several ways to address this.

You can contact the company to remove it, but you'll have to provide evidence that they made a mistake. The benefit of this approach is that their correction should be picked up by all three credit bureaus. The downside is that they have thirty days to remove it, and they may not do so.

You can also dispute the entry with the credit reporting agency itself. This is the best approach if the company doesn’t respond or the error only appears on one credit report. If both of these methods fail, you can take the matter to the Consumer Financial Protection Bureau.

Try to Remove the Correct Negative Entries

Suppose the late payment has been reported to the credit bureaus, and it is a legitimate issue. You shouldn’t dispute that as an error when it isn’t. However, you can ask the company to do a “goodwill adjustment”. After you’ve either paid the debt or entered a payment plan with the creditor, you can ask them to remove the negative entry out of “goodwill”. Note that most creditors will only do this if you have a long history of on-time payments. This means you might get a late house or car payment removed if it was truly a one-time occurrence but not if you’ve had several.

You could also negotiate a pay for delete agreement. This is a request to remove the negative entry on your credit report as a condition of repayment. However, you have to make sure that it is down on paper or else they might not hold up their part of the deal.

Monitor Your Credit Report

Unfortunately, credit reporting is an ongoing process. This means you need to constantly monitor your credit for future errors and mistakes after verifying that the entry you requested removed is gone. You may have to try another tactic if the negative entries aren’t removed or even reappear.

Conclusion

Negative entries on your credit report take up to seven years to disappear. However, there are tactics you can use to remove the negative entries, especially if you’ve corrected the situation.

Celine Hartmanshenn, Global Head of Credit from Stenn Group, an international provider of trade finance, provides her thoughts on the deficit fall.

The trade gap between China and the US is shrinking, reflecting the overall softening of global trade volumes and hinting at the movement of supply chains out of China.

US macro indicators are mixed. Unemployment remains low and prices are in check. But consumer and business spending has cooled, manufacturing output is at its lowest level in a decade, and the services sector – which accounts for 80% of economic activity – is slowing down. The lingering uncertainty stemming from the trade war and sagging global economy has caused the outlook for 2020 to dim, with the expectation of the US limping along at 1-2% GDP growth. It’s not an outright recession, but it’s certainly not a boom either.

There’s no denying that the US-China trade war is a drag on the US economy. The disruption to supply chains is expensive for businesses, the tariffs now cover a wide range of goods, and because financial markets can’t quickly adjust, they are more volatile.

So, what’s the solution? Certainly not a tariff war with the EU. The US will implement its first tariffs on aircraft and agricultural goods in 2 weeks. The EU is likely to retaliate. The aftershocks could easily tip the US into recession.

The world will be watching this month as China and the US go back to the negotiating table. Whether they like it or not, these two economies are interconnected. China is dealing with massive overcapacity, high debt levels and a need for US dollars. And the US relies on China pumping these dollars back into the US to fund its debt.

F-Secure’s Cyber ‘Threat Landscape for the Finance Sector’ shows that the sophistication of adversaries targeting banks, insurance companies, assets managers and similar organizations can range from common script-kiddies to organized criminals and state-sponsored actors. And these attackers have an equally diverse set of motivations for their actions, with many seeing the finance sector as a tempting target due to its importance in national economies.

The report breaks down these motivations into three groups: data theft, data integrity and sabotage, and direct financial theft.

“This is a useful way to think about cyber threats, because it is easy to map attacker motivations across to specific businesses, and subsequently understand to what extent they apply,” says F-Secure Senior Research Analyst George Michael. “Once you understand why various threat actors might target you, then you can more accurately measure your cyber risk, and implement appropriate mitigations.”

Data integrity and sabotage – where systems are tampered with, disrupted or destroyed – is the cyber criminals’ method of choice. Ransomware and distributed denial-of-service attacks (DDoS) are among the more popular techniques used by cyber criminals to perform these attacks.

Similar attacks have been launched by state-sponsored actors in the past. But these are less common and often linked to geopolitical provocations such as public condemnation of foreign regimes, sanctions, or outright warfare.

And while North Korea has the unique distinction of being the only nation-state believed to be responsible for acts of direct financial theft, their tactics, techniques, and procedures (TTPs) have spread to other threat actors.

According to Michael, this is part of larger trend that involves adversaries offering their customizable malware strains or services-for-hire on the dark web, contributing to a rise in the adoption of more modern TTPs by attackers.

“North Korea has been publicly implicated in financially-motivated attacks in over 30 countries within the last three years, so this isn’t really new information,” says Michael, “But their tactics are also being used by cyber criminals, particularly against banks. This is symbolic of a wider trend that we’ve seen in which there is an increasing overlap in the techniques used by state-sponsored groups and cyber criminals.”

In addition, understanding cyber threats relevant to specific organizations is crucial to being able to detect and respond to an attack when it occurs.

“Understanding the threat landscape is expensive and time-consuming,” says Michael. “If you don’t understand the threats to your business, you don’t stand a chance at defending yourself properly. Blindly throwing money at the problem doesn’t solve it either – we continue to see companies suffer from unsophisticated breaches despite having spent millions on security.”

Two thirds (66%) of people rate safe and secure payments as most important in the online checkout process, with only one in ten being most concerned about speed or simplicity. Security ranked highest across all age groups, and was a particular concern for over 55s (75%) compared to just over half of 18-24 and 25-34 year olds (52% and 53% respectively).

The survey, conducted online with YouGov, also revealed a further 76% of Brits would be willing to accept a slower or less convenient checkout experience in return for greater payment security. Meanwhile, almost half (45%) said security concerns about online payment processes were the reason most likely to put them off using a particular online retailer, more so than having to create an account (14%), a confusing process (8%), or too many steps during checkout (6%).

Keith McGill, head of ID and fraud at Equifax, said: “With more than 20% of retail revenues coming from online sales*, it’s positive to see so many consumers have security front of mind when they’re at the online checkout. The latest stats from Cifas do however show an increase in identity fraud** so it’s important shoppers remain vigilant. If you have any doubts about the professionalism of a website you should always think very carefully before entering your personal or payment details.

“New European wide regulations are on the horizon which will require two stage verification for any online purchase for more than 30 euros, similar to the security checks used for online banking. While this might feel like an extra hoop to jump through, it’s an important step forward in the ongoing battle to fight fraud.”

(Source: Equifax)

Some 55% of respondents of the survey carried out by deVere Group affirmed that they ‘regularly use financial technology to access and manage their money.’

883 people from the UK, Europe, Asia, Africa, Latin America and Australasia took part in the poll.

Of the findings, Nigel Green, deVere Group founder and CEO notes: “Even two or three years ago, that figure would have been significantly lower. The fact that today 55% of people polled globally use fintech solutions on a regular basis highlights the staggering rate of the digitalisation of our everyday lives.

“And it is speeding up. From self-driving cars, genetic bio-editing to AI, new technologies are beginning to impact every part of our lives. Our financial lives are no exception. We’re in a new age.”

He continues: “Fintech firms are filling the void left between what traditional financial services companies are offering and what customers are now expecting, especially in terms of customer experience.

“In broad terms, this means immediate, on-the-go, 24/7 access to, use and management of their money. It means personalised, on-demand services. It means lower costs.

“Fintech is already a major disruptive presence in the financial services marketplace. This trend is only set to grow as ‘digital natives’ - the first generation that grew up with the internet and smart devices – become ever more dominant in the workforce and in social and political roles.”

According to the data collected by deVere, emerging markets in Asia, Latin America and Africa are becoming the biggest growth areas for participation.

“This could be due to fintech typically offering more inexpensive solutions compared to traditional financial services. Also because these areas are home to many of the world’s 1.7 billion unbanked or underbanked population – those who don’t have access to or have limited access to financial institutions – and fintech allows this issue to be overcome,” affirms Mr Green.

Other standout trends: Around two thirds (67%) of those polled used fintech apps to send remittances and money transfers. 46% use financial technology vehicles to track investments and/or accounts. 28% use them for storing and managing cryptocurrencies.

The deVere CEO goes on to add: “Fintech – a major part of the so-called 'fourth industrial revolution' – is a positive force for three key reasons.

“First, it is meeting clear and growing client demand for on-the-go services.

“Second, it is speeding up the advance of financial inclusion across the world. Helping individuals and companies successfully manage, save and invest their money will only result in a better society for us all.

“And third, it gives firms the opportunity to diversify, cut costs, meet regulatory requirements and improve the client experience, which will help build long-term relationships and trust.”

Mr Green concludes: “The poll underscores that fintech is the new normal.”

The retail banks were responsible for the highest number of reports (486) – almost 60% of the total. This was followed by wholesale financial markets on 115 reports and retail investment firms on 53.

The root causes for the incidents were attributed to third party failure (21% of reports), hardware/software issues (19%) and change management (18%).

The FCA has recently warned of a significant rise in outages and cyber-attacks affecting financial services firms. It has also called on regulated firms to develop greater cyber resilience to prevent attacks and better operational resilience to recover from disruptions.

According to the new data obtained by RSM, there were 93 cyber-attacks reported in 2018. Over half of these were phishing attacks, while 20% were ransomware attacks.

Commenting on the figures, Steve Snaith, a technology risk assurance partner at RSM said: "While the jump in cyber incidents among financial services firms looks alarming, it's likely that this is due in part to firms being more proactive in reporting incidents to the regulator. It also reflects the increased onus on security and data breach reporting following the GDPR and recent FCA requirements.

"However, we suspect that there is still a high level of under-reporting. Failure to immediately report to the FCA a significant attempted fraud against a firm via cyber-attack could expose the firm to sanctions and penalties from the FCA.

"As the FCA has previously pointed out, eliminating the threat of cyber-attacks is all but impossible. While the financial services sector emerged relatively unscathed from recent well-publicised attacks such as NotPetya, the sector should be wary of complacency given the inherent risk of cyber-attacks that it faces.

"The figures also underline the importance of organisations obtaining third party assurance of their partners' cyber controls. Moreover, the continued high proportion of successful phishing attacks highlights the need to continue to drive cyber risk awareness among staff.

"Interestingly, a high proportion of cyber events were linked to change management, highlighting the risk of changes to IT environments not being managed effectively, leading to consequent loss. The requirements for Privacy Impact Assessments as a formal requirement of GDPR/DPA2018 should hopefully drive a greater level of governance in this area.

"Overall, there remain serious vulnerabilities across some financial services businesses when it comes to the effectiveness of their cyber controls. More needs to be done to embed a cyber resilient culture and ensure effective incident reporting processes are in place."

Fig1: The number of cyber incidents reported to the FCA by regulated firms in 2018 broken down by the sector the incident impacted (source FCA):

| Impacted sector | 2018 | % of incidents |

| Retail banking | 486 | 59% |

| Wholesale financial markets | 115 | 14% |

| Retail investments | 53 | 6% |

| Retail lending | 52 | 6% |

| General insurance and protection | 49 | 6% |

| Pensions and retirement income | 35 | 4% |

| Investment management | 29 | 4% |

| Total | 819 | 100% |

Fig2: The root causes of cyber incidents reported to the FCA (source FCA):

| Root cause | 2018 (Jan-Dec) | % of incidents |

| 3rd party failure | 174 | 21% |

| Hardware/software | 157 | 19% |

| Change management | 146 | 18% |

| Cyber attack | 93 | 11% |

| TBC | 93 | 11% |

| Human error | 47 | 6% |

| Process/control failure | 45 | 5% |

| Capacity management | 25 | 3% |

| External factors | 17 | 2% |

| Theft | 11 | 1% |

| Root cause not found | 11 | 1% |

| Total | 819 | 100% |

Fig3: The breakdown of incidents in 2018 categorised as 'Cyber attacks' (source FCA):

| Cyber attack root cause breakdown | 2018 (Jan-Dec) | % of incidents |

| Cyber - Phishing/Credential compromise | 48 | 52% |

| Cyber - Ransomware | 19 | 20% |

| Cyber - Malicious code | 16 | 17% |

| Cyber - DDOS | 10 | 11% |

| Total | 93 | 100% |

OneSpan (NASDAQ: OSPN), recently released The Future of Adaptive Authentication in the Financial Industry, a report prepared by the Information Security Media Group. Based on a broad survey of US financial institutions, the report reveals the sector’s challenges in authentication practices and strategies, and highlights the growing tension between improving security, reducing fraud and enhancing the digital customer experience.

The survey results reveal the biggest challenges stopping banks and financial institutions from being able to confidently authenticate customers and step up security include:

- 96% of organisations still rely on legacy processes tied to username and passwords for authentication;

- 44% have too many disparate tools, which are challenging to coordinate effectively;

- 44% are challenged by the use of legitimate credentials exposed in data breaches and social engineering schemes in account takeover attempts.

As a result of these challenges, more than 60% of respondents plan to invest in new multifactor authentication technologies in 2019, including those that rely on biometrics and AI/machine learning.

“The report’s findings echo what we are seeing with our customers,” said OneSpan CEO, Scott Clements. “Financial institutions are under pressure to improve their defenses against continuing and evolving threat vectors. Many are now choosing innovative technologies that dynamically respond to attacks as part of a layered security approach that stops fraud while improving the customer experience.”

The report features Aite Group’s Retail Banking and Payments Research Director, Julie Conroy, on the need for financial institutions to improve authentication methods using the latest authentication methods and technologies, including artificial intelligence, machine learning and behavioral biometrics. These emerging technologies, paired with digital identity technologies, provide a better customer experience and help financial institutions remain competitive.

The concept of sharing is so far ingrained in our everyday that most of us couldn’t imagine living in a world where we can’t share a ride, couch-surf or leave our dog with a stranger at the tap of a screen. The advancement of the sharing economy, defined by Google as an economic system in which assets or services are shared between individuals, is a prime example of this.

In fact, per the Innovation Report 2018 published by Lloyds, the global sharing economy is expected to grow to $335 billion (approximately £261 billion) by 2025. That’s considerable growth in comparison to 2014, when the estimated size of the global sharing economy was circa $15 billion (approximately £12 billion.)

This isn’t surprising when in theory the sharing economy is supposed to save resources, strengthen regional and local communities, cut costs, enable consumption for lower income groups, increase investments and provide new jobs. However, while there is a plethora of benefits to the sharing of assets and services, there is also countless risks.

In analysing Lloyd’s innovation report, British marketplace OnBuy.com wanted to share how American and British consumers feel toward the sharing economy and what they believe the risks and benefits are.

To achieve this, OnBuy designed graphics to showcase data collated by Lloyds from more than 3,000 US and UK consumers as well as representatives from 30 sharing economy companies.

In terms of benefits, both American and UK consumers believe ‘it can be cheaper for users’ - the number one benefit to the share economy, at 60% and 58% respectively.

Thereafter, it is clear American consumers are more enthused with other benefits, such as ‘it is more convenient for users’ and ‘it provides more flexibility for users’ at 52% apiece.

Comparably, just 39% of British consumers believe ‘you can earn money from your assets when you aren’t using them’. While 43% of American consumers would say the same.

In terms of risks, American consumers believe ‘there’s a risk to personal safety interacting with strangers’ which is cited as the number one risk to the share economy, at 60%.

While British consumers are caught between ‘there’s a risk to personal safety interacting with strangers’ (44%) and ‘there is no guarantee of the quality of the service or facilities (44%) in sharing their opinions on the number one risk.

Other risk factors to consider include ‘people sharing their assets could have them damaged’ (American 46%; UK 42%) and ‘people sharing their assets could have them stolen’ (American 43%; UK 41%.)

Lastly, 37% of American consumers and 33% of British consumers agree ‘there aren’t sufficient safeguards or protections in place for users’ in the sharing economy.

Cas Paton, Managing Director of OnBuy.com, comments: “If the sharing economy is to reach the proposed $335 billion mark in 2025, the industry needs to thoroughly consider the opinions of consumers. Today, the way people spend money and interact with the everyday is changing. Companies need to match this change with innovative products which meet the needs and expectations of their customers.

To combat risk, Lloyds recommends sharing economy companies partner with insurers to enhance credibility, instil confidence and build trust to drive business growth and gain a competitive advantage. I truly believe this is the way forward. Especially considering 58% of American and UK consumers currently believe the risks outweigh the benefits of using sharing economy services.”

(Source: OnBuy.com)

Almost 9 in 10 finance companies could be eligible for Research and Development (R&D) tax relief on new products and services but only 41% of them have ever claimed, Catax has revealed.

Businesses in the finance sector are missing out on millions of pounds even though 89% of them have developed new products or business process in the last two years, spending an average of £351,594 on these innovations, research shows.

This means these companies are in line for valuable R&D tax relief that the government provides to encourage innovation.

But despite three quarters (77%) of finance firms being aware of R&D tax relief, less than half report ever claiming it, the Catax study shows. This is either because they don’t think they qualify or they incorrectly believe that it is expensive and time consuming and ‘would not know where to start’.

A quarter of finance businesses do not realise they can claim R&D tax relief if they develop a new product or service while more than a third of the business managers said they ‘did not know’ if their firm had ever made a claim, according to the Censuswide survey.

The national average for the number of firms that have ever claimed is 36.8%, which puts finance companies ahead of many other sectors despite the fact they are missing out on a huge number of claims.

Executives believed the average value of an R&D tax relief claim in the first year to be just £27,254 when the true figure is almost double that, at £49,000 for firms in all sectors nationwide. R&D doesn’t even have to have been successful to qualify and claims can be backdated at least two years.

Catax CEO, Mark Tighe, commented: “The finance sector is missing out on tens of millions of pounds in R&D tax relief each year – despite claiming to be experts in finance. Many companies still think that R&D is all about science laboratories and test tubes and simply do not relate it to their own innovations.

“We need to get away from this way of thinking. The vast majority of finance companies invest hundreds of thousands each year on developing new products and services which would make them eligible and yet less than half are actually claiming.

“Finance executives looking to improve margins and efficiencies must take a proper look at their R&D tax relief entitlements. Most good R&D tax relief specialists will work on a commission basis so concerns over costs should be dismissed.

“New products and services do not even have to have been successful to quality for R&D tax relief because it is all about encouraging innovation.”

R&D tax credits can help to reduce a limited company’s corporation tax bill or be claimed as a cash sum reimbursement from the HMRC. R&D tax relief only applies to those businesses that are liable for corporation tax, including businesses making a loss.

(Source: Catax)

Following recent incidents such as TSB's systems failure and Visa's service outage, operational resilience is increasingly vital. Bank of England and FCA recently published a report stressing the importance of business continuity during a disaster. Below Finance Monthly hears from Peter Groucutt, Managing Director at Databarracks, who discusses what businesses need/can to do to strengthen their operational resilience during a disaster to absorb any shock a business may experience.

In July 2018, the Bank of England, Prudential Regulation Authority (PRA) and Financial Conduct Authority (FCA) published a joint discussion paper aimed at engaging with the financial services industry to improve the operational resilience of firms and financial market infrastructures (FMIs).

At the time it was issued, banks and FMI’s were capturing media attention, following several high-profile incidents.

TSB’s failed IT migration has been well publicised, costing the firm £176.4m in various fees and leading to the departure of its chief executive, Paul Pester. In June 2018, shortly before the release of this paper, millions of people and businesses were unable to pay for shopping due to a sudden failure of Visa’s card payment system.

Financial services lead in business continuity

The financial services industry is a leader in business continuity and operational resilience. It has a requirement of a high level of systems-uptime and is well-regulated. The best practices it introduces are often taken and more widely adopted by other industries. Our own research supports this. Our annual Data Health Check survey provides a snapshot of the IT industry from the perspective of over 400 IT decision-makers. The findings from this year’s survey provided some revealing insights.

64% of financial institutions had a business continuity plan in place, compared to an industry average of 53%. Of the financial sector firms with a specific IT disaster recovery process within their business continuity plan, 64% had tested this in the past 12 months – compared to 47% across other industries. Finally, 81% of financial firms had tested their IT disaster recovery plans against cyber threats, versus 68% of firms in other sectors.

While these findings reinforce the strength of the industry’s operational resilience, incidents like TSB and Visa prove it is not immune to failures.

The regulators want to “commence a dialogue that achieves a step-change in the operational resilience of firms and FMIs”. The report takes a mature view to the kind of incidents firms may face and accepts that some disruptions are inevitable. It provides useful advice that can be taken and applied not only to the financial services community, but other industries too.

Leveraging advice to improve operational resilience

So, what can be learned from this report? Firstly, setting board-approved impact tolerances is an excellent suggestion. This describes the amount of disruption a firm can tolerate and helps senior management prioritise their investment decisions in preparation for incidents. This is fundamental to all good continuity planning; particularly as new technologies emerge, and customer demand for instant access to information intensifies. These tolerances are essential for defining how a business builds its operational practices.

Additionally, focusing on business services rather than systems is another important recommendation. Designing your systems and processes on the assumption there will be disruptions – but ensuring you can continue to deliver business services is key.

It’s also pleasing to see the report highlight the increased concentration of risk due to a limited number of technology providers. This is particularly prevalent in the financial sector for payment systems, but again there are parallels with other industries and technologies. Cloud computing, for example, it’s reaching a state of oligopoly, with the market dominated by a small number of key players. For customers of those cloud services, it can lead to a heavy reliance on a single company. This poses a significant supplier risk.

Next steps

Looking ahead, the BoE, PRA and FCA have set a deadline of Friday 5th October for interested parties and stakeholders to share their observations. The supervisory authorities will use these responses to inform current supervisory activity, helping to dictate future policy-making. The supervisory authorities will then share relevant information with the Financial Policy Committee (FPC), supporting its efforts to build resilience in the financial system.

Firms looking to improve their operational resilience should take advantage of this excellent resource – whether in financial services or not.