Navigating the complexities of auto and student loans is crucial for long-term financial stability in the U.S.

Many Americans rely on these financial products to purchase vehicles, pursue higher education, and invest in their future. Yet, understanding how to manage interest rates, repayment obligations, and eligibility criteria is essential to avoid unnecessary debt and maximize financial opportunities. This guide provides a detailed, section-by-section analysis of both auto and student loans, offering actionable strategies, key insights, and the latest data to help borrowers make informed decisions.

How to Get the Best Rate on an Auto Loan

Securing the best rate on an auto loan begins with a comprehensive understanding of your credit profile and financial situation. Credit scores are a primary determinant in the rates lenders offer, with higher scores generally translating into lower interest rates. According to Bankrate, as of September 2025, the average interest rate for a 60-month new car loan was 7.21%, but borrowers with excellent credit could qualify for rates as low as 5.25%. Borrowers with lower credit scores often face rates above 12%, which significantly increases the overall cost of financing a vehicle.

Beyond credit scores, your debt-to-income ratio and income stability play crucial roles in determining loan approval and terms. Lenders examine these factors closely to assess your ability to make consistent payments. Preparing your financial documentation in advance, including proof of income, tax returns, and existing debt obligations, can streamline the approval process. Additionally, shopping around between banks, credit unions, and online lenders can reveal better rates and terms. Pre-approval is also a valuable strategy; it allows you to understand your financing capacity and gives leverage during negotiations at dealerships.

The term length of your auto loan also affects the interest rate. Shorter loans typically have higher monthly payments but lower total interest, while longer loans reduce monthly payments at the cost of paying more in interest over time. Making a larger down payment further reduces the principal amount, improving your chances of obtaining a competitive rate. Ultimately, careful planning and comparison can save thousands of dollars over the life of the loan and make purchasing a vehicle far more affordable.

The Benefits of Refinancing Your Student Loans

Refinancing student loans can be a powerful tool to manage debt, especially for borrowers who have improved their financial situation since graduation. By consolidating multiple loans into a single loan with a lower interest rate, borrowers may reduce their monthly payments and the total interest paid over the life of the loan. According to recent data from the Federal Reserve, Americans hold over $1.67 trillion in student loan debt, with the average borrower owing approximately $39,075. Refinancing can make this debt more manageable, particularly for borrowers with high-interest private loans.

However, refinancing federal loans into a private loan eliminates federal protections, such as access to income-driven repayment plans and loan forgiveness programs. Borrowers must weigh the benefits of a lower interest rate against the potential loss of these protections. Refinancing can be particularly beneficial for borrowers with strong credit histories who have secured stable employment and are confident in their ability to maintain consistent payments.

Additionally, private lenders may offer flexible repayment terms, allowing borrowers to tailor the loan to their financial goals. Careful evaluation of refinancing options ensures that borrowers make decisions aligned with both short-term affordability and long-term financial planning.

Understanding the Financial Aid Process for College in the U.S.

Applying for college financial aid in the United States is a structured process, starting with the Free Application for Federal Student Aid (FAFSA). The FAFSA collects detailed financial information to determine a student's eligibility for federal grants, loans, and work-study programs. States and many colleges also use FAFSA data to award institutional aid. Once submitted, students receive a Student Aid Report (SAR) summarizing their information, which must be reviewed for accuracy. Errors in reporting income or assets can affect eligibility, so careful attention is necessary.

Colleges then issue financial aid offers, detailing the types and amounts of aid available, which may include federal loans, grants, scholarships, or work-study opportunities. Understanding the terms of these offers is critical; grants and scholarships do not require repayment, whereas loans do, often with interest rates that vary based on whether they are federal or private. Students and families should compare offers carefully, considering factors such as loan repayment terms, expected monthly payments after graduation, and potential income-driven repayment plans. Strategic financial planning can reduce long-term debt and ensure that educational investments remain manageable.

A toy car ascends a stack of coins, illustrating how auto loan rates and borrowing costs can impact U.S. car buyers’ finances.

A Guide to Auto Loan Interest Rates: Fixed vs. Variable

Auto loans are available with fixed or variable interest rates, each with distinct advantages and risks. Fixed rates remain constant throughout the loan term, providing predictable monthly payments and protecting borrowers from market fluctuations. This predictability aids in budgeting and is often preferred by those planning to keep their vehicles long-term.

Variable rates, by contrast, fluctuate with market conditions. They often start lower than fixed rates, which can reduce initial monthly payments, but carry the risk of increases over time. Borrowers considering variable rates should assess economic trends and their own financial flexibility to ensure they can accommodate potential rate increases. The Federal Reserve’s adjustments to interest rates, inflation, and employment data all influence variable loan rates, making them somewhat unpredictable. Borrowers should weigh the potential cost savings against the uncertainty to choose the best option for their financial situation.

The Pros and Cons of a Private Student Loan

Private student loans can help bridge the gap when federal aid isn’t enough to cover college costs. These loans often come with higher borrowing limits than federal loans, allowing students to finance more expensive programs or out-of-state tuition. For borrowers with strong credit histories or a co-signer with excellent credit, private lenders can offer competitive interest rates. In 2025, the average private student loan interest rate ranged from 5% to 12% depending on creditworthiness and lender terms.

However, private loans have significant drawbacks. Unlike federal loans, they generally lack income-driven repayment options and deferment protections, leaving borrowers fully responsible for repayment regardless of financial circumstances. Many private loans also have variable interest rates, which can increase over time and raise monthly payments.

Additionally, the approval process heavily depends on credit scores, employment history, and debt-to-income ratios, making it harder for borrowers with weaker financial profiles to secure favorable terms. Careful consideration of these factors is crucial before committing to a private student loan, as it can impact long-term financial health.

Navigating the Federal Student Loan Repayment System

Repaying federal student loans requires understanding the variety of repayment plans available. The standard repayment plan, spanning 10 years, offers fixed monthly payments and is the default option for most borrowers. This plan ensures predictable payments and faster debt elimination but may be challenging for those with lower post-graduation income.

Income-driven repayment (IDR) plans, including Income-Based Repayment (IBR) and Pay As You Earn (PAYE), calculate monthly payments based on income and family size. These plans can make payments more manageable, particularly for borrowers in lower-paying fields, and may extend repayment up to 20 or 25 years.

At the end of that term, any remaining balance may be forgiven, though it may be considered taxable income. Graduated and extended repayment plans provide additional flexibility, allowing payments to start lower and increase over time or extending the term for those with larger balances. Staying informed about loan forgiveness programs, deferment, and forbearance options is essential to avoid default and optimize repayment strategies.

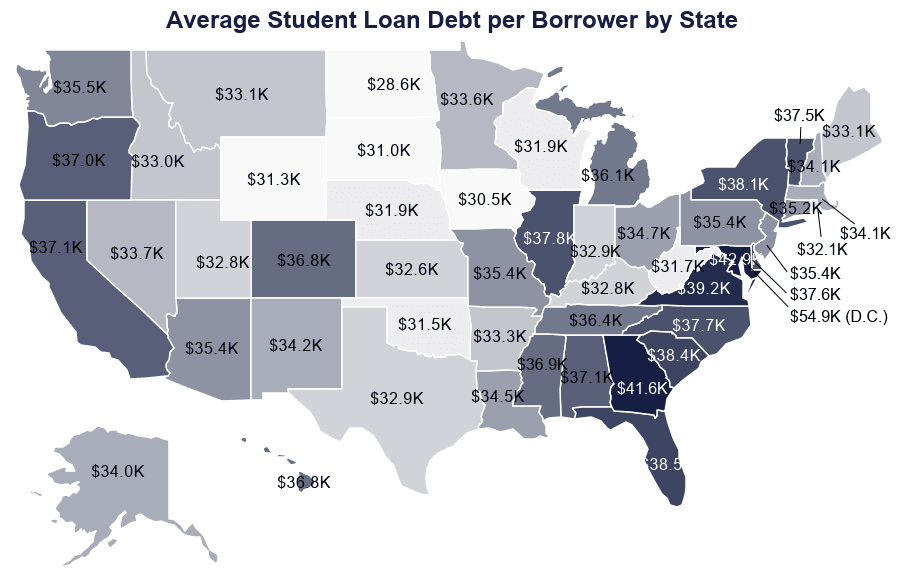

This map highlights the average student loan debt across each U.S. state, showing how college costs and borrowing vary regionally for American students.

How to Buy a Car with Bad Credit in the United States

Buying a car with bad credit is challenging but achievable with careful planning. Reviewing your credit report is the first step, ensuring all information is accurate and identifying areas for improvement. Even small corrections to your credit report can impact the rates lenders offer. In 2025, borrowers with credit scores below 600 faced average auto loan rates above 14% for new vehicles, illustrating the importance of understanding your credit profile before applying.

A larger down payment can improve approval odds and reduce the total interest paid. Additionally, shopping around among lenders that specialize in high-risk borrowers is crucial. Some credit unions and online lenders offer more competitive terms than traditional banks. Using a co-signer with stronger credit can also enhance approval chances and secure a lower interest rate. Borrowers should carefully budget to ensure monthly payments remain manageable, as missing payments can further harm credit scores and reduce future borrowing options.

Is a Car Lease Right for Your Business?

Leasing a vehicle for business purposes can offer lower monthly payments and the ability to drive newer models more frequently. Lease payments are generally smaller than loan payments, freeing up capital for other operational needs. Businesses can sometimes deduct lease payments as a tax expense, providing additional financial benefits.

However, leases come with restrictions, such as mileage limits and penalties for excessive wear and tear. Overstepping these limits can result in costly fees at the end of the lease term. Moreover, a leased vehicle remains the property of the leasing company, meaning businesses do not build equity in the asset. Companies should assess vehicle usage, anticipated mileage, and long-term cost implications to determine whether leasing aligns with operational goals and financial strategy.

What Happens If You Default on a Student Loan?

Defaulting on a student loan can have serious financial and legal consequences. Federal student loans enter default after 270 days of non-payment. Once in default, the full loan balance becomes due immediately, and the government may garnish wages, withhold tax refunds, and add collection fees. A defaulted loan is also reported to credit bureaus, severely damaging the borrower’s credit score and limiting access to new credit for years.

Private student loan defaults have similar consequences, including legal action to recover the debt. Borrowers facing financial hardship should proactively contact their loan servicer to explore deferment, forbearance, or income-driven repayment options. Addressing repayment challenges early can prevent default and protect creditworthiness. Understanding the repercussions of default and planning for repayment ensures long-term financial stability.

The Impact of U.S. Economic Trends on Auto Loan Rates

Auto loan rates are highly sensitive to broader U.S. economic trends. The Federal Reserve’s monetary policy decisions, such as raising or lowering the federal funds rate, directly influence borrowing costs. As of September 2025, the Fed maintained rates between 4% and 4.25% to curb inflation while supporting economic growth according to Investopedia.

Inflation, employment levels, and consumer confidence also affect loan rates. High inflation often leads to increased rates, while strong employment can boost consumer borrowing, impacting supply and demand dynamics for auto loans. Additionally, vehicle demand influences rates, as high demand can tighten financing availability, increasing rates, whereas slower markets may offer more competitive financing options. Borrowers should monitor these economic indicators to strategically time vehicle purchases or refinancing opportunities.

A graduation cap sits atop $100 bills, symbolizing the financial burden of student loans and the investment required for a college education in the U.S.

People Also Ask

Many borrowers have common questions about auto and student loans in the United States. Understanding these issues can help in planning and managing debt effectively.

What is the average student loan debt in the U.S.?

As of 2025, the average federal student loan debt per borrower is approximately $39,075, with the total outstanding student loan balance reaching $1.67 trillion.

How can I improve my credit score to get a better auto loan rate?

Paying bills on time, reducing outstanding debt, and disputing inaccuracies on credit reports are essential steps. A stronger credit score can substantially lower the interest rate on auto loans.

Are there government programs to help with student loan repayment?

Yes. Income-driven repayment plans and Public Service Loan Forgiveness (PSLF) provide options for reducing monthly payments or forgiving remaining debt after meeting eligibility requirements.

Can I refinance my student loans with bad credit?

Refinancing is possible but challenging with poor credit. Federal loans offer income-driven plans, while private refinancing may require a co-signer or result in higher interest rates.

What happens if I default on my student loan?

Defaulting triggers wage garnishment, damaged credit, collection fees, and the potential loss of eligibility for federal financial aid. Proactive communication with loan servicers can prevent default.

Conclusion

Auto and student loans are integral components of financial planning in the United States. By understanding how interest rates are determined, exploring refinancing options, navigating repayment systems, and monitoring economic trends, borrowers can make informed decisions that optimize financial outcomes. Whether purchasing a vehicle, financing higher education, or managing existing debt, strategic planning, careful research, and proactive financial management are essential for maintaining long-term financial health.