Choosing between secured and unsecured personal loans can shape your financial future, impacting everything from interest rates to approval chances.

Understanding the differences between these two lending options is essential for anyone looking to borrow responsibly and strategically. Personal loans are one of the most versatile borrowing tools available to U.S. consumers. They can be used for debt consolidation, home improvements, medical bills, or even major life events.

As of Q2 2025, the most recent data from the Federal Reserve's G.19 Consumer Credit report indicates that U.S. banks issued approximately $40.1 billion in personal loans. This figure reflects a steady increase in personal loan issuance, highlighting the growing role of banks in household finance.

The choice between a secured and unsecured loan remains a significant decision for borrowers, each offering distinct benefits, risks, and financial implications. Understanding these differences is crucial for aligning the appropriate type of loan with individual financial needs and circumstances.

Secured Loans Explained

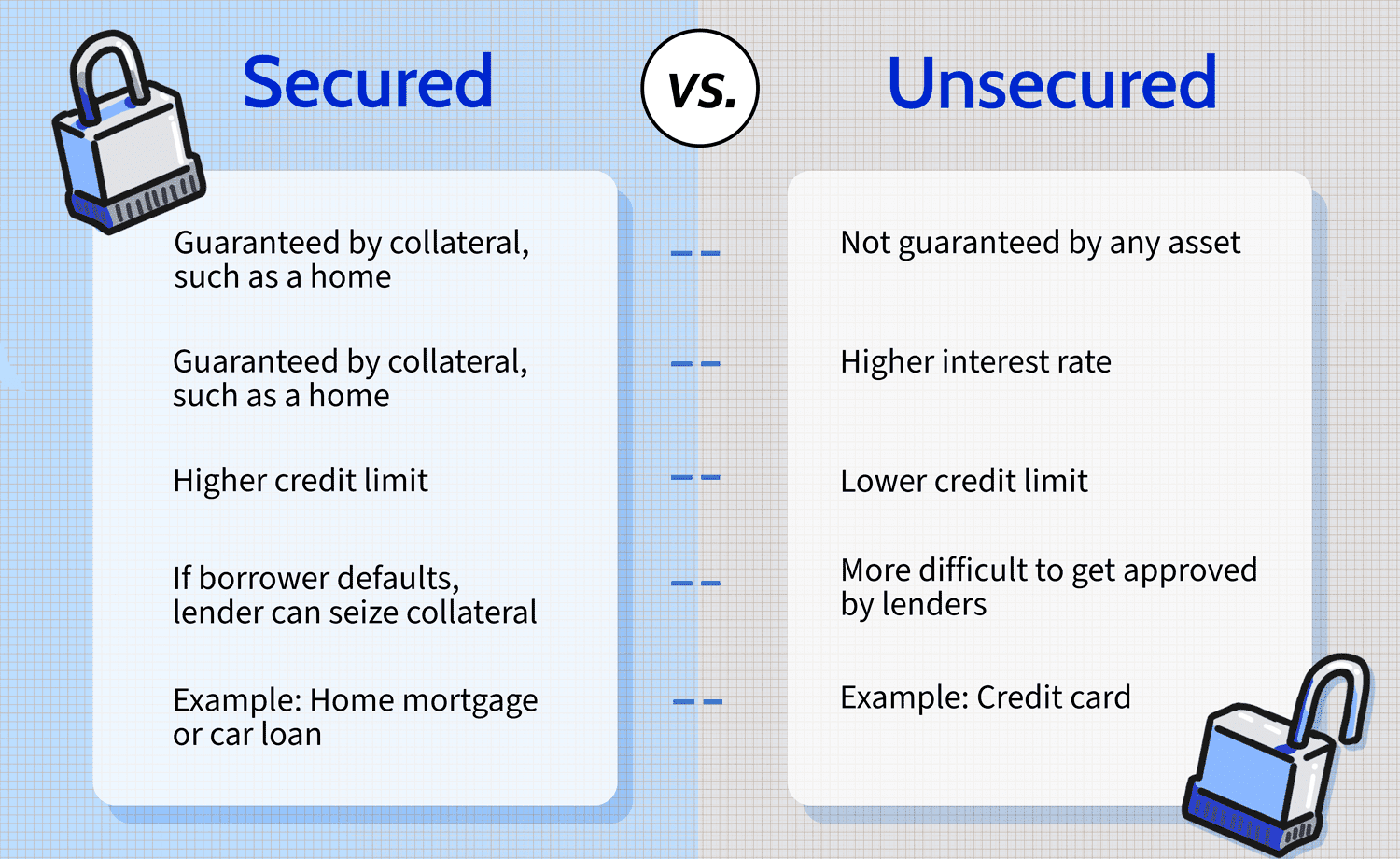

A secured loan is tied to an asset, meaning the lender can claim that property if the borrower defaults. Most commonly, this asset is a home, but in practice, collateral can also include cars, jewelry, or other valuables.

Because the lender carries less risk, secured loans generally come with lower interest rates, larger borrowing limits, and longer repayment terms compared to unsecured borrowing. U.S. lenders typically allow homeowners to borrow up to 80–85% of their property’s appraised value, minus any outstanding mortgage balance, when taking out a home equity loan or second mortgage.

While secured loans make it easier to access larger amounts of credit—even for borrowers with weaker credit scores or self-employed income—the trade-off is significant. If payments are missed, the lender can repossess the collateralized asset, potentially putting a borrower’s home or vehicle at risk.

This makes secured borrowing a double-edged sword: powerful for debt consolidation or major investments but dangerous if financial stability is uncertain. In addition, many secured loans run over longer periods, which can increase the total interest paid. Data from Experian shows that U.S. secured personal loan balances average over $18,000, compared to roughly $8,000 for unsecured personal loans, underscoring the larger commitments typically involved.

Unsecured Loans Explained

Unsecured loans, often referred to as personal loans, do not require collateral. Instead, approval depends on a borrower’s creditworthiness, income, and overall financial history. Because lenders shoulder more risk in this arrangement, unsecured loans usually carry higher interest rates and lower borrowing limits.

The Federal Reserve’s consumer credit report for 2024 shows that the average interest rate for a 24-month unsecured personal loan stood at 12.49%, compared to mortgage rates below 7% and secured loan rates that can fall much lower.

While unsecured borrowing offers flexibility and reduces the risk of losing physical assets, borrowers must stay disciplined. Missing payments may result in late fees, penalties, and negative marks on credit reports, which can significantly reduce FICO® scores.

In cases of serious delinquency, lenders also retain the right to pursue repayment through civil court action, which can add legal costs and long-term consequences to an already burdensome debt. Still, for borrowers with strong credit profiles, unsecured loans remain a popular choice. The most recent data from TransUnion indicates that 28.8 million consumers in the U.S. held unsecured personal loans.

This represents a significant increase from the previous quarter, where the number was 23.9 million. The growth is attributed to factors such as rising credit card balances and increased borrowing among younger consumers.

A visual guide to understanding the key distinctions between secured and unsecured loans, helping borrowers choose the right option.

Key Differences in Terms and Eligibility

The approval process for secured loans is generally more lenient, as the collateral offsets the lender’s risk. This makes them accessible to borrowers with less-than-perfect credit. In contrast, unsecured loans require stronger credit histories. Borrowers with credit scores above 720 secured unsecured personal loan rates as low as 10.5% in 2024, while those below 640 often faced rates above 20%.

Borrowing limits also differ. Secured personal loans can sometimes exceed $100,000 depending on collateral, while unsecured loans typically max out around $50,000. Repayment terms vary but generally range from 12 to 84 months for both loan types.

Risks and Considerations

While secured loans offer better interest rates, the risk of losing an asset can have long-term consequences. If a borrower defaults, repossession or foreclosure can leave lasting damage both financially and emotionally. On the other hand, unsecured loans protect assets but can quickly become burdensome if taken at high interest rates. Missing payments may lead to collections, lawsuits, and significant credit score damage.

Borrowers should weigh whether lower rates are worth the collateral risk. The Consumer Financial Protection Bureau (CFPB) emphasizes the importance of evaluating repayment ability before borrowing, particularly for secured loans tied to essential assets like vehicles or homes.

People Also Ask

What is the main advantage of a secured personal loan?

The primary advantage is lower interest rates and higher borrowing limits, made possible by collateral.

Can unsecured loans help build credit?

Yes. Making on-time payments on an unsecured loan can improve your credit score over time, showing lenders you are a reliable borrower.

Which loan is easier to get approved for?

Secured loans are generally easier to qualify for because collateral reduces the lender’s risk, making them more accessible to borrowers with weaker credit.

Are interest rates fixed or variable on personal loans?

Both secured and unsecured loans can carry fixed or variable interest rates. Fixed rates provide predictable payments, while variable rates can fluctuate with market conditions.

Can I convert an unsecured loan into a secured one?

In some cases, lenders may allow borrowers to secure an existing loan with collateral to reduce interest rates, but this depends on lender policy and borrower eligibility.

Conclusion

The decision between a secured and unsecured personal loan depends on your financial situation, goals, and risk tolerance. Secured loans may be ideal for borrowers seeking larger amounts and lower rates, provided they are comfortable pledging collateral. Unsecured loans, while potentially more expensive, offer speed, simplicity, and protection of personal assets.

By carefully considering your credit standing, repayment ability, and long-term financial strategy, you can choose the loan type that best aligns with your needs. In today’s evolving credit landscape, understanding the nuances of secured versus unsecured borrowing is not just about accessing funds—it’s about building a stronger financial future.