The financial landscape for businesses in the United States in 2025 is more dynamic than ever, offering CEOs a diverse array of financing options beyond the traditional banking system.

Alternative lending has surged in popularity, driven by technological advancements and a growing demand for flexible, accessible capital. From peer-to-peer lending platforms to fintech-driven solutions, microloans, and digital banks, these alternatives are empowering businesses—particularly small and medium-sized enterprises and startups—to fuel growth, innovate, and navigate economic challenges.

This comprehensive guide explores the most relevant alternative lending and financial strategies available to U.S. CEOs, providing actionable insights to make informed decisions. By understanding the mechanics of these options, addressing ethical considerations, and fostering strong lender relationships, business leaders can build resilient financial frameworks that drive long-term success and competitive advantage in an evolving market.

A CEO's Guide to P2P (Peer-to-Peer) Lending Platforms

Peer-to-peer lending has transformed into a cornerstone of alternative financing, revolutionizing how businesses access capital by connecting borrowers directly with investors through digital platforms, bypassing traditional banking intermediaries. Precedence Research shows that in 2025, the global P2P lending market is valued at approximately USD 176.5 billion and is projected to reach USD 1,380.80 billion by 2034, with a compound annual growth rate of 25.73%, according to Precedence Research. This growth is driven by innovations like AI-driven credit scoring and blockchain for secure transactions.

In the U.S., platforms such as LendingClub, Prosper, and Funding Circle cater to businesses of varying sizes, offering loans from a few thousand to millions of dollars based on creditworthiness. These platforms use data analytics for faster approvals and competitive rates compared to banks, but challenges like platform fees (1-6% of the loan amount) and higher default risks for weaker credit profiles persist. Regulatory uncertainty also looms as the P2P framework evolves.

To succeed, CEOs should maintain strong credit profiles, compare platform terms, and diversify funding sources to mitigate risks. By leveraging P2P lending strategically, businesses can secure capital quickly and cost-effectively, enabling them to seize growth opportunities and address financial needs with agility.

How to Use Lending to Fuel Your Business's Growth

Strategic borrowing can propel business growth by enabling expansion, innovation, and liquidity in a competitive economy. In 2025, small business loans, commercial real estate, residential mortgages, and commercial and industrial loans are key revenue drivers for community banks, as noted by Independent Banker. CEOs should align loans with objectives like market expansion or technology investments.

Evaluating loan terms is crucial to ensure alignment with financial capacity. Fixed-rate loans offer predictability, while variable-rate loans may have lower initial rates but risk increases. Repayment schedules and collateral requirements also impact cash flow and asset risk. Effective cash flow management, supported by detailed forecasts and a debt service coverage ratio of at least 1.25, ensures debt obligations are met without straining operations.

By treating loans as growth tools, CEOs can leverage borrowed capital for sustainable success, balancing strategic investments with financial discipline to achieve long-term goals.

The Ethical Considerations of Predatory Lending in the US Market

Predatory lending, characterized by exploitative interest rates and unfair terms, remains a significant concern in the U.S. In 2024, 45 states and the District of Columbia implemented caps on loan fees, per the National Consumer Law Center, but varying protections allow high fees in some states, trapping borrowers in debt cycles. This particularly affects small businesses and underserved communities.

CEOs must prioritize ethical lending practices to protect their companies and stakeholders, educating teams about predatory signs like hidden fees or aggressive tactics. Advocating for fair lending laws and working with reputable lenders fosters trust and safeguards reputations.

Ethical due diligence, including thorough loan agreement reviews, is essential to mitigate risks. By upholding transparency and integrity, businesses can navigate the financial landscape responsibly and maintain stakeholder confidence.

A CEO carefully examines financial statements to make informed decisions for his company’s growth and strategy.

Exploring Fintech's Role in Modernizing the Lending Industry

Fintech companies are revolutionizing lending with technology-driven solutions, accounting for $500 billion in global loans in 2025, a fraction of the $18 trillion U.S. household debt. Innovations like AI credit scoring and blockchain payments enhance speed and transparency. Embedded finance, such as buy-now-pay-later, reshapes capital access.

Platforms like Kabbage and OnDeck offer automated applications and rapid approvals, streamlining financing. However, data privacy and reliance on technology pose risks. CEOs can benefit from tailored financial products by partnering with reputable fintech providers, improving efficiency and competitiveness.

Staying informed about fintech trends allows businesses to leverage these tools for financial agility, balancing innovation with careful risk management to optimize lending processes.

A Guide to Microloans for American Entrepreneurs

Microloans are a lifeline for startups and small businesses, providing accessible capital for those ineligible for traditional loans. In 2023, the Small Business Administration issued $87 million in microloans, supporting over 5,500 businesses, with 35% aiding Black-owned and 15% Latino-owned businesses, per the SBA. These loans, ranging from $500 to $50,000, fund early-stage projects or operations.

Entrepreneurs should prepare robust business plans and understand eligibility criteria to secure approval. Strategic use of funds for marketing or inventory can build a strong foundation and improve credit for future financing. Working with SBA-approved lenders ensures favorable terms.

Microloans empower entrepreneurs to launch and sustain ventures, offering a critical stepping stone for growth in a competitive market.

The Art of the Loan Negotiation: Tips for Securing Favorable Terms

Negotiating favorable loan terms is critical for optimizing financing strategies in 2025. CEOs must assess their financial position, including revenue and debt, to present a strong case to lenders. Comparing offers from banks, P2P platforms, and fintech providers leverages competition for better terms.

Professional advice from financial or legal experts helps navigate complex agreements, avoiding pitfalls like prepayment penalties. Building lender relationships through transparency and reliability enhances negotiating power. Thorough preparation ensures terms align with business goals.

By approaching negotiations with knowledge and confidence, CEOs can secure flexible, cost-effective loans, supporting financial stability and strategic growth.

How to Leverage a Trust or LLC for Financial Lending

Legal structures like trusts and LLCs offer advantages in securing loans by enhancing credibility and flexibility. Trusts protect assets, while LLCs provide liability protection and tax benefits, appealing to lenders. Clear operating agreements and proper documentation demonstrate stability.

Consulting legal professionals ensures compliance with regulations, strengthening creditworthiness. These entities can access larger credit lines and better terms while protecting assets. Leveraging trusts or LLCs creates a robust financial framework.

Businesses benefit from increased lender confidence and strategic financial planning, enabling growth with reduced personal and corporate risk.

Understanding the Credit Repair Process in the US

A strong credit profile is vital for securing favorable loan terms. In 2024, the U.S. credit repair industry generated $6.6 billion, per ConsumerAffairs, reflecting demand for credit improvement. CEOs can boost credit by reviewing reports for errors, paying bills on time, and reducing debt.

Disputing inaccuracies and maintaining low credit utilization improves scores. Reputable credit repair agencies can guide recovery from setbacks, but vetting providers avoids scams. Proactive credit management enhances borrowing capacity.

Strong credit positions businesses for better terms and financial stability, supporting long-term success in a competitive landscape.

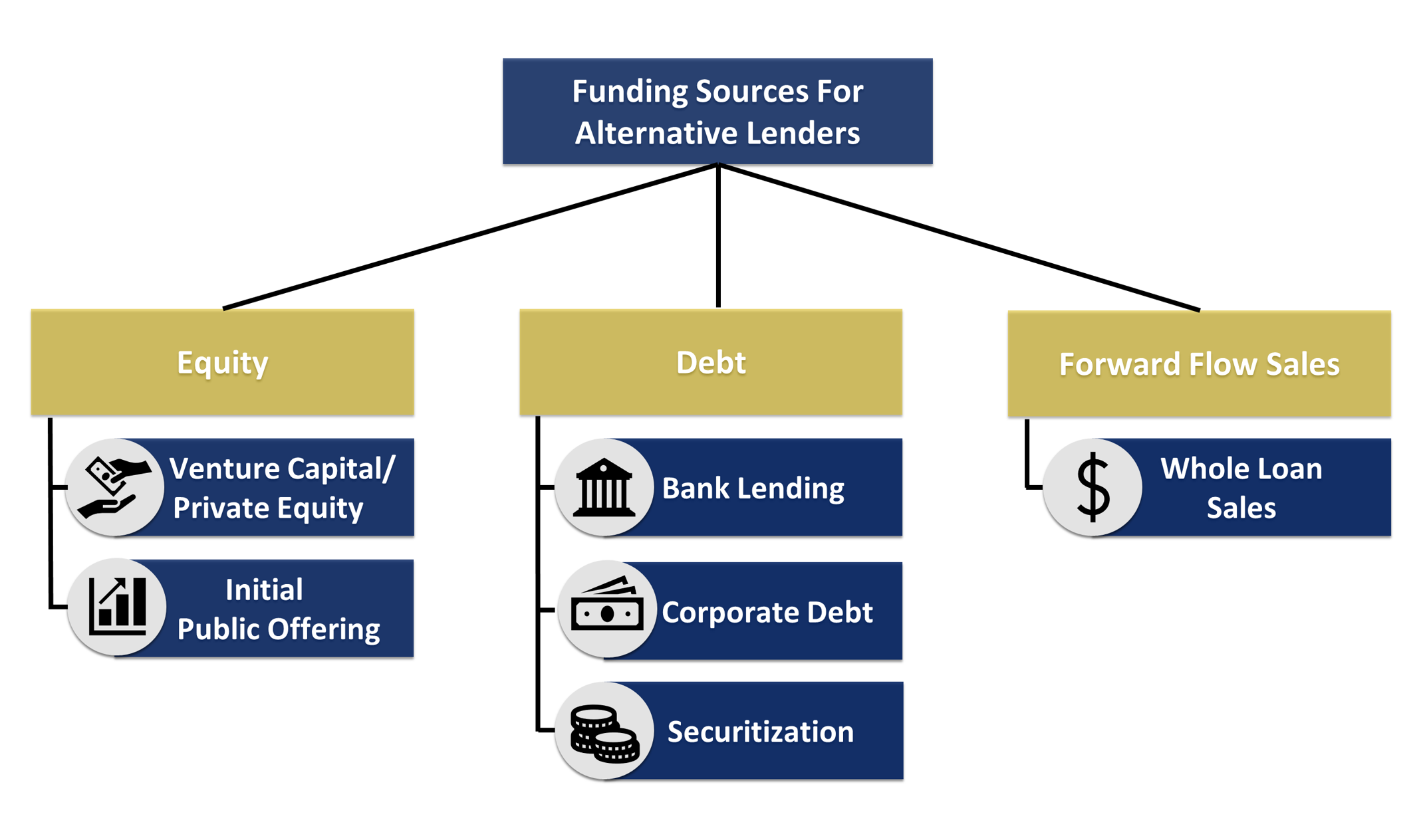

A visual guide to various lending methods, helping businesses and entrepreneurs understand financing options at a glance.

The Future of Lending: What CEOs Can Expect from Digital Banks

Digital banks are reshaping lending with hyper-personalization and cryptocurrency integration in 2025. AI and machine learning enable faster approvals and customized products, while mobile-first platforms enhance accessibility. These innovations meet modern business needs.

However, digital banks may lack personalized service, and technology reliance raises data security concerns. Partnering with reputable providers unlocks tools like real-time analytics, improving decision-making. Staying informed about trends ensures alignment with business goals.

CEOs can leverage digital banks for efficient capital access, balancing innovation with security to drive financial agility.

Why Every Business Should Have a Strong Relationship with a US Bank Lender

Despite alternative lending’s rise, strong relationships with U.S. bank lenders remain vital. In 2025, community banks anticipate growth in small business and commercial loans, per Independent Banker. These relationships offer larger credit lines and preferential terms.

Transparency and timely repayments build trust, unlocking financial advice and additional services like treasury management. Banks provide stability during economic uncertainty, complementing alternative financing. Regular communication strengthens partnerships.

By balancing traditional and alternative approaches, CEOs ensure financial support and resilience, driving sustainable growth.

People Also Ask

What is alternative lending in the US?

Alternative lending refers to non-traditional financing methods, including peer-to-peer lending, fintech platforms, microloans, and online lenders that operate outside conventional banks.

How can CEOs use loans to grow their business?

Loans can fund expansion, technology investments, and operational scaling, but CEOs should weigh the cost of capital against projected returns to ensure profitability.

What are the risks of predatory lending?

Predatory lending exposes businesses to excessive interest rates, unfair terms, and reputational damage. Ethical due diligence and regulatory awareness are critical to mitigate risks.

Are microloans suitable for startups?

Yes, microloans provide smaller capital injections ideal for startups, helping them build credit and fund essential early-stage projects.

How are digital banks changing lending?

Digital banks offer faster approvals, AI-driven credit assessments, and mobile-first platforms, enabling CEOs to access capital more efficiently.

Conclusion

Alternative lending and financial strategies provide U.S. CEOs with a versatile toolkit to access capital, manage risks, and drive growth in 2025. Peer-to-peer lending, fintech innovations, microloans, and digital banks offer flexible solutions tailored to diverse needs. Ethical standards, strong credit profiles, and robust lender relationships are essential for success. Combining traditional banking’s stability with alternative options’ agility enables businesses to build resilient financial frameworks, ensuring sustainable success and a competitive edge in an evolving economic landscape.