Debt consolidation is more than just a financial maneuver—it is a pathway to reclaiming stability and reducing stress in an increasingly complex credit environment.

With U.S. household debt surpassing $18.2 trillion, non-mortgage debt averaging $21,800 per adult, and credit card interest rates often exceeding 20%, Americans are navigating a challenging landscape of payments and financial obligations according to the Federal Reserve. Debt consolidation provides an opportunity to merge multiple debts into a single manageable payment, potentially lowering interest rates and simplifying monthly obligations.

Beyond financial relief, consolidation offers psychological benefits by organizing debts into one clear plan, reducing anxiety and providing a roadmap toward long-term financial stability. Borrowers should also consider how their FICO score impacts loan eligibility and interest rates, especially when using Personal Loans for consolidation.

Understanding Debt Consolidation

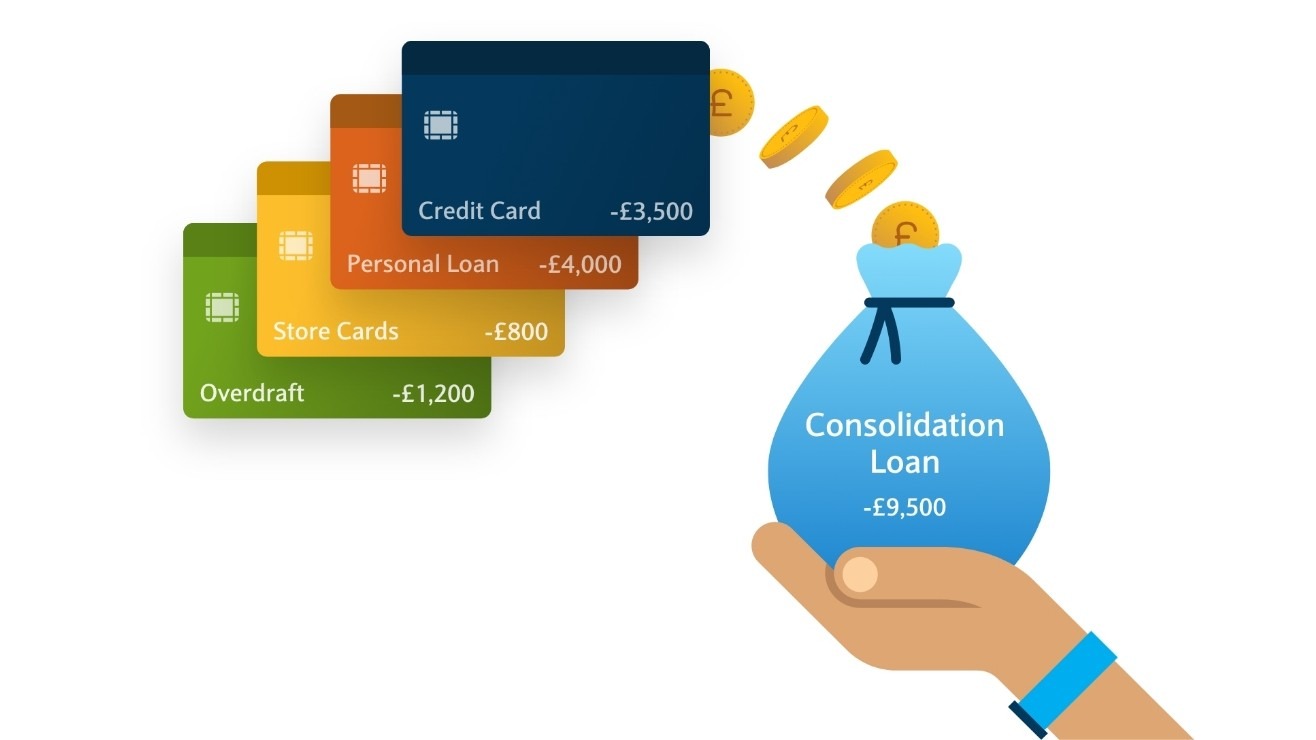

Debt consolidation occurs when an individual combines several outstanding debts into one new loan, creating a single monthly payment. This can include credit card balances, personal loans, medical bills, or other unsecured obligations. The goal is to simplify repayment while possibly reducing interest rates and creating a predictable schedule.

Consolidation can take multiple forms: personal loans from banks, credit unions, or online lenders; balance transfer credit cards with introductory low or zero percent APRs; or home equity loans that leverage existing property as collateral. Each method carries specific benefits, requirements, and risks, making it essential to choose a strategy aligned with your financial profile and repayment capacity.

Some borrowers may also consider a Home Equity Line of Credit (HELOC) as a consolidation option, using the equity in their home to pay off higher-interest debts while potentially benefiting from lower interest rates—though it is important to understand the risks of putting your home at stake.

The Consolidation Process: Step by Step

A successful consolidation plan begins with a detailed understanding of your current debts. Start by listing all balances, interest rates, monthly payments, and remaining terms for each account. Reviewing a current credit report from one of the major credit bureaus—TransUnion, Experian, or Equifax—ensures accuracy and reveals your creditworthiness.

Once debts are clearly documented, research consolidation options, comparing rates, fees, loan terms, and repayment schedules. Personal loans often feature fixed rates and predictable monthly payments, while balance transfer cards may offer temporary interest-free periods, provided your credit qualifies and the transfer limit covers your total balances without negatively impacting your credit utilization. For those with strong credit scores, balance transfers can provide significant interest savings, but careful planning is necessary to avoid accruing new debt on old accounts.

Simplifying finances by consolidating multiple debts into one manageable loan can reduce stress and streamline repayment.

Benefits of Debt Consolidation

Beyond the simplification of payments, debt consolidation can reduce financial strain and improve overall money management according to Experian. Consolidation can lower interest rates, particularly when high-interest credit cards are replaced by a lower-rate loan. Combining multiple debts into one payment reduces the likelihood of missed or late payments, which in turn can strengthen credit scores over time.

Moreover, the psychological benefit of having a single, organized payment schedule cannot be overstated: borrowers often report reduced stress and a greater sense of control over their finances. By freeing mental bandwidth previously consumed by multiple deadlines and statements, individuals can focus on budgeting, saving, and planning for long-term goals.

Risks and Considerations

Debt consolidation is not a guaranteed solution. Borrowers must maintain disciplined repayment habits; otherwise, they risk accumulating new debt alongside the consolidated loan. Certain consolidation methods, such as home equity loans or balance transfer credit cards, may carry fees, interest rate changes, or collateral risk.

Longer repayment terms may reduce monthly obligations but increase total interest paid over time, while shorter terms require higher monthly payments. Additionally, missing payments on the new loan can negatively impact credit scores, potentially undoing any prior progress. A thorough evaluation of income, expenses, and financial discipline is essential before pursuing consolidation to ensure the chosen method aligns with both immediate needs and long-term financial goals.

Strategic Repayment Methods After Consolidation

Once debts are consolidated, the method of repayment significantly influences success. Borrowers may choose the debt avalanche method, prioritizing repayment of the highest-interest debt first, minimizing total interest paid.

Alternatively, the debt snowball method focuses on paying off the smallest balances first, providing early psychological wins and motivation. A hybrid approach, the debt blizzard method, begins with the smallest balances before targeting the highest-interest debts, combining the benefits of both strategies. Selecting a repayment strategy that complements your financial habits and maintains momentum is critical for maximizing the benefits of consolidation.

When to Seek Professional Guidance

Professional guidance can enhance the consolidation process. Accredited financial counselors, nonprofit credit agencies, and reputable online lenders offer advice on repayment strategies, loan selection, and budgeting.

Credit counseling agencies may offer debt management plans, negotiating reduced interest rates and waived fees with creditors while providing structured repayment schedules. Borrowers should also exercise caution to avoid scams, such as services demanding upfront fees or promising unrealistic results. Researching lender reputations and reading reviews from the Better Business Bureau or Consumer Financial Protection Bureau can prevent potential pitfalls.

People Also Ask

If you’re considering debt consolidation, these questions often come to mind and can guide your decision-making process.

How does debt consolidation impact my credit score?

Debt consolidation can improve your credit score by lowering credit utilization and streamlining payments, but missing payments or accumulating new debt can have negative effects.

Are there risks associated with debt consolidation loans?

Yes. Borrowers must consider potential fees, collateral risks, and interest rate changes. Longer repayment terms may reduce monthly payments but increase total interest costs.

What is the difference between a consolidation loan and a debt management plan?

A consolidation loan replaces multiple debts with a single loan, while a debt management plan consolidates payments without creating a new loan, often through a credit counseling agency.

Can anyone qualify for a balance transfer card?

No. Strong credit is typically required, and the card limit must be high enough to accommodate all transferred balances without negatively impacting your credit utilization ratio.

What repayment method is most effective after consolidation?

The most effective method depends on your goals and habits. The debt avalanche minimizes interest paid, the debt snowball builds momentum through small wins, and the debt blizzard combines both strategies for balance and motivation.

Conclusion

Debt consolidation is a powerful tool for Americans seeking to regain control over their finances, reduce interest costs, and simplify complex debt obligations. By carefully evaluating debt, selecting the most suitable consolidation method, and implementing disciplined repayment strategies, borrowers can improve credit performance, decrease financial stress, and achieve long-term financial stability.

When combined with strategic budgeting and professional guidance, debt consolidation not only manages existing debt but also establishes a framework for lasting financial resilience.