Earning more money doesn’t always make you wealthier — unless you know how to stop your spending from rising just as fast.

In 2025, many Americans are earning higher salaries than they did just a few years ago, yet financial stress remains widespread. The reason? Lifestyle inflation — the gradual increase in discretionary spending that occurs when income rises. Between 2022 and 2023, U.S. consumer spending grew by nearly 6% across all income brackets, while only around half of adults (54%) had enough savings to cover three months of expenses, according to recent financial surveys. In other words, as people earn more, they’re spending nearly all of it — and saving little.

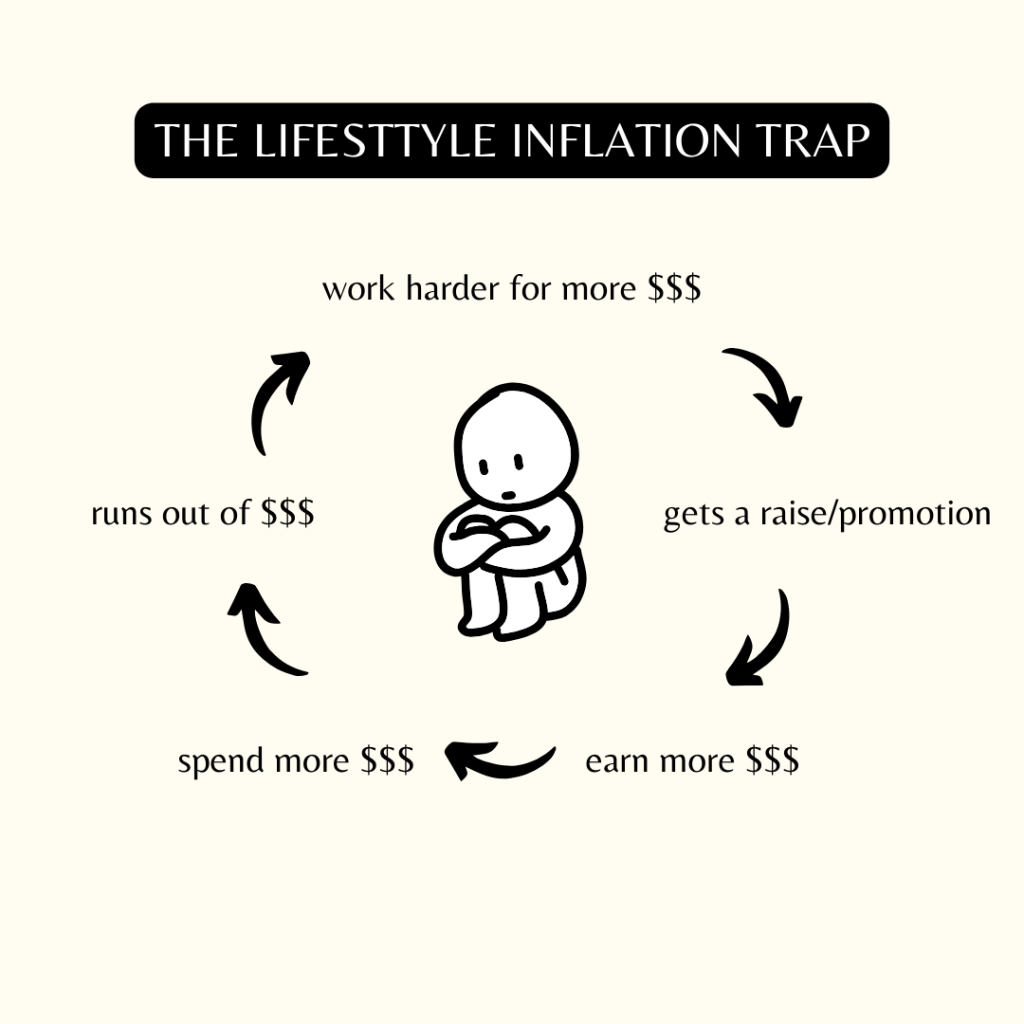

Lifestyle inflation, also called lifestyle creep, is not inherently negative. A better income should improve your quality of life. But without boundaries, those upgrades — pricier meals, larger homes, luxury subscriptions — can quietly erode the long-term wealth you’re working so hard to build. Understanding the psychology behind this tendency is the first step to mastering it.

The Emotional Triggers Behind Lifestyle Inflation

Spending more as you earn more is often a psychological reflex, not a financial decision. Behavioral economists link this to hedonic adaptation — the human tendency to quickly get used to new comforts, prompting the need for constant upgrades to feel the same satisfaction.

For example, the first time you stay in a luxury hotel, it feels special; by the fifth time, it feels normal. That same pattern applies to everyday purchases — cars, clothes, gadgets, and even homes. Psychologists also note the influence of social comparison: as peers post their upgrades on social media, people subconsciously feel pressure to “keep up.”

Studies by Richard Thaler and Cass Sunstein (authors of Nudge) show that these biases aren’t due to weakness but wiring. Humans are hardwired to adapt and benchmark against others. The challenge, then, isn’t just to resist temptation but to redesign your environment so saving and investing happen automatically.

The Numbers: How Americans Spend More as They Earn More

Recent data from the Bureau of Economic Analysis (BEA) and Federal Reserve show that U.S. personal saving rates have fallen dramatically since their 2020 pandemic highs — hovering around 4% in mid-2025, compared to over 20% during the height of lockdowns. Meanwhile, real wages have increased for many sectors, particularly in technology, healthcare, and finance.

Yet, according to Bankrate, about one in three Americans continues to live paycheck to paycheck, even among households earning over $100,000 per year. A growing number of people are carrying record levels of credit card debt, which surpassed $1.1 trillion nationally in early 2025. These figures underscore that higher earnings often translate to higher spending — not greater stability.

Why “Treat Yourself” Isn’t Always a Trap

A healthy lifestyle upgrade isn’t inherently bad. If you’ve worked for years to afford a nicer home, better healthcare, or experiences that improve your wellbeing, that’s money well spent. The key lies in balance: intentional improvement vs. automatic expansion.

Think of it like this: upgrading your life with purpose is financial progress; upgrading it out of habit is financial drift. As Investopedia’s 2025 analysis suggests, the problem arises when small indulgences — premium coffee, streaming bundles, upgraded tech — silently stack into major financial leaks. Over time, these “invisible upgrades” can consume thousands of dollars annually, money that could otherwise grow through compounding investments.

The Real Cost of Lifestyle Creep: Compounding in Reverse

Consider a 30-year-old who gets a $10,000 raise. If they direct half of that raise ($5,000 per year) into a 401(k) earning an average annual return of 7%, they could accumulate over $500,000 by age 60. But if that same $5,000 goes to new expenses — car leases, gadgets, eating out — it’s gone forever.

The difference is not just arithmetic, it’s psychological. People tend to frame spending as deserved rewards, but they rarely calculate what that money could have become. As one financial planner aptly puts it, “Every dollar you don’t invest today is a future version of yourself that has fewer choices.”

When income rises but savings don’t, the cycle of lifestyle inflation can leave even high earners feeling trapped and financially stressed.

How to Rewire the Psychology of Spending

Breaking free from lifestyle inflation doesn’t mean cutting all joy from your budget. It means aligning your spending with your values and putting structure around how raises, bonuses, and windfalls are used. Here’s how the most financially resilient Americans are doing it in 2025:

1. Automate your progress

Set up direct transfers so a portion of each raise automatically goes into savings or investments. Treat it like a non-negotiable bill. Studies show that automation increases long-term savings rates by over 40%, according to research from Vanguard and the Consumer Financial Protection Bureau.

2. Create a “raise rule”

Before you see a salary bump in your paycheck, decide where it will go. Many advisors recommend the 50-30-20 split: 50% toward financial goals (investments, debt repayment, or emergency fund), 30% for lifestyle improvements, and 20% for taxes or buffer savings.

3. Revisit your emotional triggers

Identify what drives your spending — stress, comparison, boredom, or the feeling of success. Journaling or tracking your “why” behind major purchases can reveal surprising patterns that help you curb impulse decisions.

4. Define your financial comfort zone

Lifestyle creep often happens when people fail to define “enough.” Decide in advance what “comfortable” means for you — in terms of housing, transportation, and leisure — so you don’t endlessly escalate your expectations.

5. Build safety nets before luxuries

According to Bankrate’s 2024 emergency savings survey, only 44% of Americans could cover an unexpected $1,000 expense without borrowing. Before upgrading anything, ensure your emergency fund covers at least 3–6 months of expenses.

People Also Ask

Is lifestyle inflation always bad?

Not necessarily. Lifestyle improvements that genuinely add value or support your wellbeing can be positive. The danger lies in unconscious spending that trades future freedom for short-term gratification.

How can I stop lifestyle creep after a raise?

Use the “invisible raise” approach: automatically divert a portion of each raise into savings before it hits your account. If you never see it, you won’t miss it.

What are early warning signs of lifestyle inflation?

Frequent impulse buys, subscription creep, and declining savings contributions are early red flags. Tracking monthly savings percentages rather than dollar amounts can make inflation easier to spot.

How does lifestyle creep affect retirement?

Even modest inflation in your personal lifestyle can delay retirement by years. Each dollar spent today is one that can’t grow through compound interest over decades.

Conclusion: Awareness Is the Real Luxury

Lifestyle inflation thrives on autopilot. The moment you start paying attention to where your extra income goes, you’ve already taken control. Americans in 2025 are earning more but saving less — proof that the difference between financial stress and financial freedom isn’t income; it’s intention.

By setting clear goals, automating your savings, and making every upgrade a conscious choice, you transform money from something that slips away to something that works for you. True wealth isn’t about spending more — it’s about buying yourself more time, security, and peace of mind.