Your credit score is more than just a number — it’s the key that unlocks (or locks) your financial future in America.

Credit scores quietly shape the most important financial moments of our lives: whether we get the mortgage, the auto loan, the best credit card, or even that job in finance. In 2025 the credit landscape is changing — not only because household debt and delinquency patterns are shifting, but because scoring models, bureau practices, and credit-building products (like Experian Boost and secured cards) have evolved.

This article gives you a step-by-step, practical roadmap for understanding credit scoring in the United States, checking and interpreting reports, fixing errors, and improving your score efficiently and sustainably. Wherever possible I back up recommendations with current U.S. data and link to authoritative sources so you can verify and act with confidence.

What Is a Credit Score and Why Does It Matter in the US?

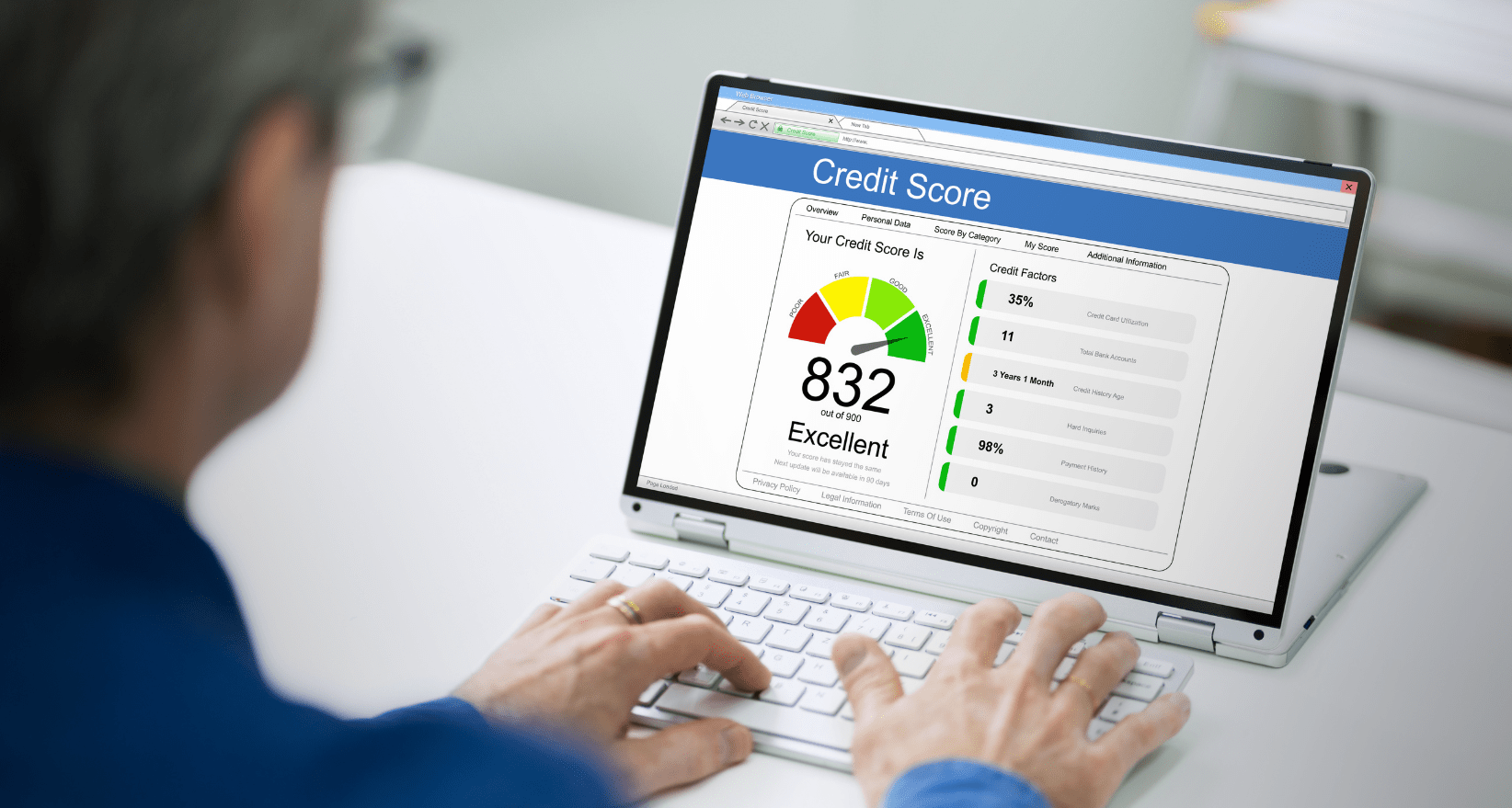

A credit score is a three-digit summary of the information in your consumer credit file that lenders use to estimate credit risk. In the U.S., lenders overwhelmingly use FICO® scores (though VantageScore is also common in some contexts). The average FICO® Score in 2025 is roughly 715, but the distribution varies by state — Minnesota and some New England states trend highest while parts of the Southeast are lower. Your score matters because it directly affects loan approval odds, interest rates, insurance premiums, and sometimes employment or housing prospects; a small difference in score can mean thousands of dollars over the life of a mortgage or auto loan.

FICO and other scoring systems weigh payment history, amounts owed (utilization), length of credit history, new credit, and credit mix. Of these, on-time payments and utilization generally have the largest immediate effects. Recent changes such as renewed reporting of student loan delinquencies have moved the national average and made timely payments even more critical in 2025.

How to Check and Interpret Your Credit Report

You have three major credit reports in the U.S.: Equifax, Experian, and TransUnion. Federal law entitles you to access your reports for free via AnnualCreditReport.com; many services now offer free weekly or monthly monitoring as well. When you pull a report, prioritize these checks: identity details (name, SSN), account status (open/closed), payment history codes, balances and credit limits, public records (liens, judgments), and inquiries. Look for negative marks that are older than the legally allowed time (most negative items fall off after seven years; bankruptcies can remain longer). Errors are common—studies and consumer advocacy research find material mistakes or inaccuracies at surprisingly high rates—so treat every discrepancy seriously.

Interpreting a report means translating listings into impact. An open card with a zero balance is an asset to utilization; a 30-day late payment is a red flag and lowers scores significantly according to MarketWatch. Charge-offs, collections, and 90+ day delinquencies have outsized negative effects. If you find an error, document it, file a dispute with the bureau online and by certified mail if necessary, and follow up until it’s corrected. Keep copies of correspondence. Tools such as the bureau dispute portals, and consumer-facing apps that aggregate bureau data, make monitoring simpler but don’t replace the annual deep check.

The Difference Between FICO and VantageScore Explained

FICO is the historic industry standard and remains the score most lenders reference; VantageScore is a widely available alternative created by the major bureaus. The two models use similar factor categories (payment history, utilization, etc.) but they differ in weighting, scoring ranges (both commonly use 300–850 now), and data rules (for example, newer VantageScore versions are more likely to score “thin” files and can incorporate alternative payment data more readily).

In practice, a borrower might see a modest spread between their FICO and VantageScore because of differences in how medical collections, authorized user tradelines, or very recent account openings are handled. For lenders, FICO still dominates mortgage and many mainstream credit decisions, but VantageScore’s ability to score consumers with thinner files has made it useful for certain products and prequalification tools. If you’re monitoring scores, check both when possible and ask prospective lenders which model they use so you know which number matters for a given loan.

Requesting a credit report is the first step toward understanding your financial standing and protecting your credit health.

How to Improve Your Credit Score Fast: US Edition

“Fast” is relative: some actions can move your score in weeks, others take months. The highest-impact immediate moves are lowering utilization and curing late payments. Paying down a large portion of revolving balances before the statement closing date can reduce the reported utilization and often produces a visible score bump within one or two billing cycles. Bringing past-due accounts current (even by payment plans) removes the most damaging ongoing factor—payment history.

Use Experian Boost or equivalent services judiciously: registering regular utility and phone payments can trigger incremental increases for some consumers by adding positive payment history to the Experian file. Opening a small secured card and keeping the balance low while making on-time payments can also produce gains over 3–6 months. Avoid applying for multiple new accounts in a short period; hard inquiries shave points and multiple inquiries suggest higher risk to scoring models. If you have high-interest credit card debt, moving it to a 0% introductory balance transfer (and paying aggressively) reduces interest drag and lowers utilization. For many people, combining these tactics—paying down balances, bringing accounts current, adding a secured product, and avoiding new hard pulls—can produce the most rapid, measurable improvements.

Common Credit Report Errors and How to Dispute Them

Errors on credit reports range from identity mix-ups and outdated balances to mistaken late payments and misreported bankruptcies. Consumer studies and investigative reporting have repeatedly documented error rates that justify vigilance: a sizable minority of consumers find at least one meaningful mistake on their reports during spot checks.

When you find an error, gather documentation supporting your claim (bank statements, payoff letters, identity documents) and submit a dispute to the reporting bureau(s) showing the inaccuracy. The bureaus must investigate and respond under the Fair Credit Reporting Act, typically within 30 days. If the bureau does not correct an error, escalate to the creditor and then to the Consumer Financial Protection Bureau (CFPB) if needed. Keep a written trail of every communication. Fixing errors often yields immediate benefits because a corrected late payment or removed collection can restore dozens of points to a score.

The Impact of Credit Inquiries on Your Score

Credit inquiries come in two types: soft and hard. Soft inquiries (prequalification checks, self-checks) have no effect on scores. Hard inquiries—when a lender checks your credit as part of an application—typically lower scores by a small amount (often 5–10 points) and remain visible for two years, though they usually only affect scores meaningfully for the first year.

Rate shopping for a mortgage, auto loan, or student loan is treated differently by many scoring models: multiple hard inquiries of the same type within a short “shopping” window (usually 14–45 days depending on the model) are grouped and count as a single inquiry to minimize penalizing smart comparison shopping. Still, avoid unnecessary applications, and when comparison shopping for loans, do it within a compressed time window to minimize score impact. If you see unexpected hard inquiries on your report, dispute them—fraudulent or unauthorized inquiries must be removed.

How Credit Utilization Affects Your Credit Rating

Credit utilization (the percentage of your available revolving credit that you use) is the second-most important factor in most scoring models after payment history. The conventional guidance is to keep utilization under 30% overall and on each card, though lower utilization—10% or less—often correlates with stronger scores. Utilization is reported at statement closing dates, so paying down balances prior to that date (not just before the due date) is essential to change what the bureaus see.

High utilization signals risk even if payments are on time; conversely, low utilization demonstrates capacity to borrow responsibly. If you carry substantial balances for business or short-term reasons, consider requesting a credit limit increase (which raises available credit and lowers utilization if balances stay steady) or moving balances across cards to distribute utilization more evenly. However, requesting a limit increase may trigger a hard pull with some issuers, so ask whether the issuer will perform a hard or soft inquiry before requesting.

Understanding where your credit score falls—from Excellent to Very Poor—can help you anticipate personal loan interest rates and borrowing options.

Building Credit with Secured Credit Cards

Secured credit cards provide a reliable path to establish or rebuild a positive credit history. These cards require a refundable deposit that typically becomes your credit limit; for example, a $300 deposit creates a $300 limit. Use the secured card for a modest recurring charge you can pay in full each month—this produces on-time payment history and reported low utilization.

Over 6–12 months, a pattern of responsible use can qualify you for an unsecured card or a product upgrade with the issuer. Compare secured cards for reporting policies (does the issuer report to all three bureaus?), fees, and upgrade path. Some secured cards now offer rewards or automatic reviews for graduation to unsecured status. For consumers emerging from significant derogatory history, a secured card plus a small credit-builder loan (with payments reported to the bureaus) is one of the fastest, lowest-risk ways to generate positive tradelines.

How to Rebuild Credit After Bankruptcy

Bankruptcy is a serious event for credit files, but it’s also a legal reset that many people use to rebuild stronger finances. Chapter 7 bankruptcies typically stay on a credit report for 10 years, while Chapter 13 tends to remain for 7 years; however, the biggest negative effect fades after a few years if the consumer demonstrates good behavior according to the Federal Register.

The quickest path back includes establishing positive payment history (secured cards, credit-builder loans), maintaining low utilization, and adding installment products with steady payments (for example, an auto loan or small personal loan) that are paid on time. Be cautious with “quick fix” products that charge high fees; instead choose mainstream secured cards from reputable issuers, and ask creditors to report positive payment arrangements when possible. Many people see meaningful score improvement within 12–24 months if they maintain disciplined behaviors and avoid new derogatory marks. Also, be proactive: after bankruptcy, ensure any discharged debts are marked correctly on reports and dispute incorrect lingering collections.

Understanding “Credit Mix” and Why It Matters

Credit mix refers to the variety of credit types on your report—revolving (credit cards) versus installment (mortgages, auto loans, student loans). A healthy credit mix demonstrates to lenders that you can manage different kinds of credit responsibly. It’s typically a lower-weight factor compared with payment history and utilization, but for some borrowers (particularly those with thin files) adding a small installment account can improve scores faster than other methods because it creates a diversified payment record.

That said, never take on installment debt solely for scoring purposes; the economic cost of unnecessary loans generally outweighs the modest scoring benefit. Where appropriate—such as financing a necessary car purchase—treat installment accounts as an opportunity to build long-term positive history.

People Also Ask

How often should I check my credit report?

Check full credit reports from each bureau at least once per year via AnnualCreditReport.com, and use monitoring tools for alerts; many services allow free weekly checks to catch identity theft or errors early.

Can closing a credit card hurt my score?

Yes. Closing a long-held account reduces your average account age and lowers available revolving credit—both can raise utilization and lower score. Consider keeping low-cost, long-established accounts open and use them occasionally to prevent closure.

Will paying collections remove the negative mark?

Paying a collection reduces future risk but may not automatically remove the negative entry. Negotiate a pay-for-delete only when the collection agency agrees in writing; otherwise, paying may simply change status to “paid” but the record can still affect scores. Dispute inaccuracies aggressively.

How long do hard inquiries affect my credit?

Hard inquiries typically have their largest impact within the first year and remain on the file for two years; multiple inquiries for the same loan type within a short window are often grouped and treated as one to facilitate rate shopping.

Shot of a stressed out young couple using a Facing financial stress, this couple reviews their credit card statement and bills, unsure how to manage rising debt.

Conclusion

Mastering credit scores and reports in the U.S. requires both understanding and discipline. The fundamentals remain simple: pay on time, keep utilization low, monitor your reports, dispute errors, and build a credit history that demonstrates reliability across account types. In 2025, the environment demands extra vigilance—student loan reporting resumed, delinquency patterns are shifting, and credit models are evolving—but the same common-sense strategies produce results.

Use the tools available (free reports, boost features, secured products, and nonprofit counseling when necessary), make a prioritized action plan, and check progress regularly. With consistent effort, you can both repair damage and prepare your credit profile for the next major financial step, whether that is a mortgage, a business loan, or a new job that relies on your financial reputation.