This article may contain affiliate links.

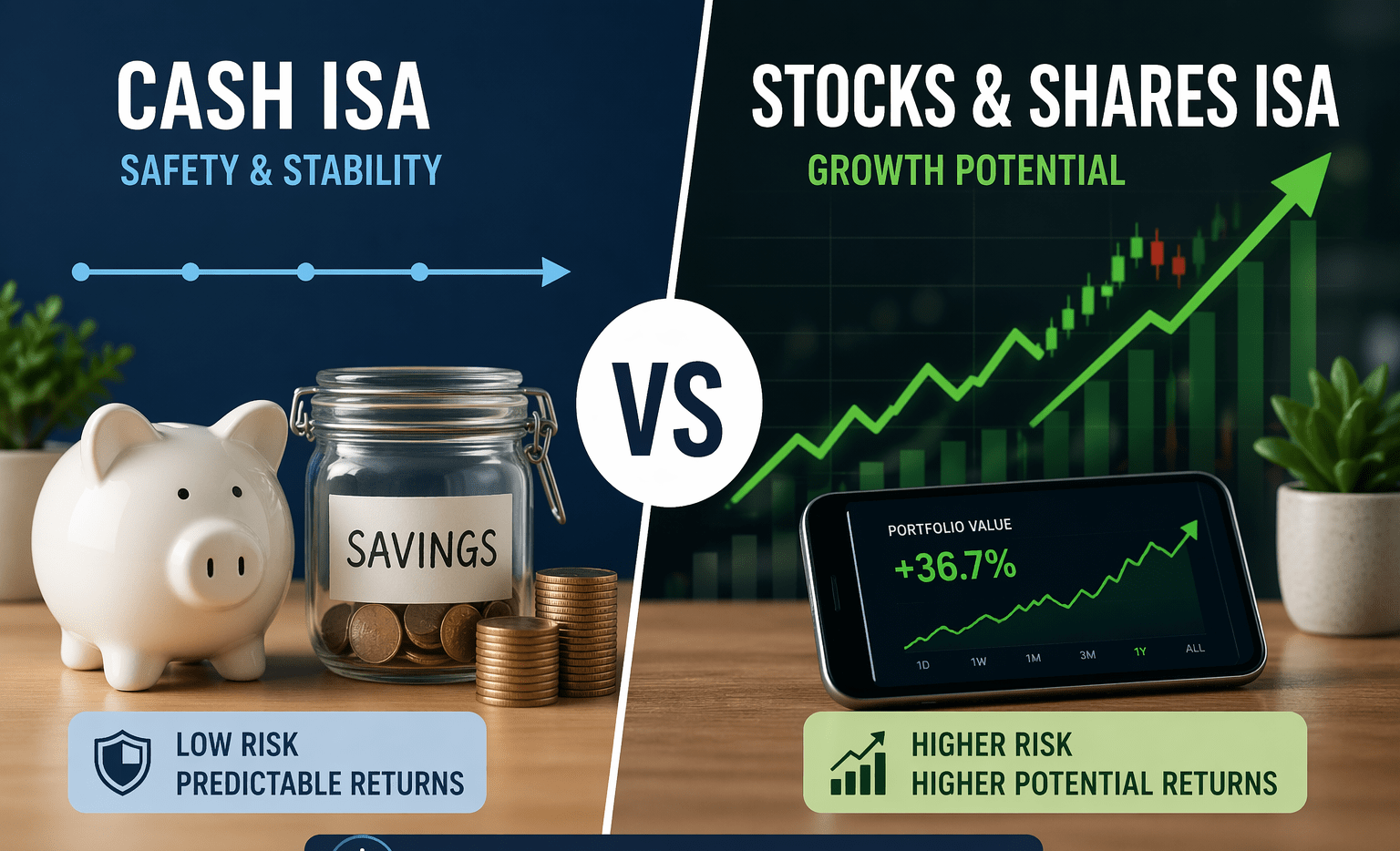

Cash ISAs are back—but that’s exactly why more savers are starting to question whether staying in cash is actually costing them in the long run.

For a closer look at current rates and how Cash ISAs are changing in 2026, see our guide to Cash ISAs.

Rates of 4–5% look strong on the surface. But over time, they don’t solve a bigger problem: how money actually grows.

A Stocks and Shares ISA can be worth it in 2026 for long-term investing, but it comes with risk—and it isn’t designed for short-term savings.

That trade-off is what more people are now actively weighing.

What a Stocks and Shares ISA Actually Does

A Stocks and Shares ISA is a tax-efficient investment account that allows you to put money into assets like shares, ETFs, bonds, and funds without paying UK income tax or capital gains tax on any returns.

The tax advantage is the same as a Cash ISA. The difference lies in how those returns are generated.

With cash, interest tends to sit within a relatively narrow range. With a Stocks and Shares ISA, returns depend on market performance. That creates more potential for growth, but it also introduces uncertainty, particularly over shorter periods.

Why Stocks and Shares ISAs Are Surging in 2026

There’s a noticeable shift happening this year. More investors—especially those using app-based platforms—are moving towards Stocks and Shares ISAs rather than relying entirely on cash.

Part of this is a reaction to higher interest rates. While better returns have made cash more attractive again, they’ve also made its limitations more visible over time. For savers thinking beyond the next year or two, the question is no longer just about protecting money, but what it can realistically grow into.

There’s also growing awareness around how ISA allowances work. With £20,000 available each year—and uncertainty around how those limits might evolve—more people are choosing to use their allowance fully while they can.

At the same time, providers are competing more aggressively. Many modern platforms now combine investing tools, simple interfaces, and ISA wrappers in one place, making it easier for newer investors to get started without needing multiple accounts.

Taken together, this is shifting behaviour. The conversation is moving from understanding ISAs to actively deciding how to use them.

Is It Worth Getting a Stocks and Shares ISA?

That depends largely on time horizon.

For money you may need in the short term, a Stocks and Shares ISA can feel unpredictable. Markets move, sometimes sharply, and those fluctuations don’t always align with near-term plans.

Over longer periods, however, the dynamic changes. This is where investing has historically outperformed cash—not because it avoids risk, but because it has greater capacity to grow.

In practice, this is why many savers are no longer treating cash and investing as an either/or decision. Instead, they’re using them alongside each other, balancing stability with growth depending on their goals—an approach explored in more detail in Cash ISA vs Stocks and Shares ISA UK 2026: Which Is Better for Your Money?.

For some, that also extends beyond traditional investing into more active approaches, such as Copy Trading UK: Is It a Good Idea or Too Risky in 2026?, which introduces a different way of accessing markets—alongside a different set of risks.

What Are the Disadvantages of a Stocks and Shares ISA?

The main drawback is exposure to market risk.

Unlike a Cash ISA, where returns are relatively stable, the value of investments can rise and fall. In the short term, that can mean seeing your portfolio drop in value, sometimes unexpectedly.

There’s also no guaranteed return. Even diversified investments depend on broader market conditions, and outcomes can vary depending on timing and strategy.

Costs are another factor to consider. Platforms like eToro aim to keep pricing straightforward, with flat trading fees and capped custody charges, but fees still exist and can affect overall performance over time.

None of these are unusual. They simply reflect the trade-off between stability and growth.

How Much Do You Need in an ISA to Earn £1,000 a Month?

This is one of the most common questions—and one without a simple answer.

Because returns aren’t fixed, the amount required depends on the rate of return achieved over time.

To give a rough illustration:

- £1,000 per month equals £12,000 per year

- At a 5% annual return, that implies around £240,000 invested

- At a 7% return, it drops closer to £170,000

These figures are purely illustrative, but they highlight an important point. Generating consistent income at that level typically relies on both substantial capital and a long-term investment approach, rather than short-term positioning.

Can You Put £20,000 in Both a Cash ISA and a Stocks and Shares ISA?

No—the £20,000 ISA allowance applies across all ISA types combined.

That means you can choose how to allocate it. You might put the full amount into a Stocks and Shares ISA, keep it entirely in cash, or split it between the two.

What you can’t do is contribute £20,000 to each separately within the same tax year.

Transfers, however, are treated differently. Moving an existing ISA to another provider does not count towards your annual allowance. This gives savers the flexibility to switch platforms or reorganise their accounts without affecting their tax-free limit.

How Platforms Are Changing the Way People Invest

Accessibility has improved significantly in recent years, and that’s changing how people approach investing.

Platforms like eToro allow users to build and manage portfolios within a single ISA wrapper, with access to a wide range of UK, US, and European assets. Instead of relying on multiple providers, investors can view and adjust their holdings in one place.

There’s also more flexibility around how accounts are structured. ISA transfers allow existing investments to be moved without losing their tax advantages, and some platforms offer incentives on qualifying deposits or transfers, which can reduce the friction of getting started.

For savers looking to move beyond cash without overcomplicating things, this kind of setup is increasingly becoming a practical starting point—particularly for those who want control alongside tax efficiency.

Final Thought

Stocks and Shares ISAs aren’t new, but the way people are using them is changing.

Higher cash rates have brought savings back into focus, yet they’ve also made the limits of cash more apparent over time. That shift is prompting more savers to think beyond short-term returns and consider how their money works over longer periods.

The result isn’t a move away from cash, but a more balanced approach—one that recognises the different roles each option plays.

And that’s ultimately where the decision sits in 2026. Not simply whether a Stocks and Shares ISA is worth it, but whether relying on cash alone still makes sense.

FAQ

What is a Stocks and Shares ISA?

A tax-efficient account that allows you to invest in assets like shares, ETFs, and funds without paying UK tax on returns.

Is a Stocks and Shares ISA risky?

Yes. Investments can go down in value as well as up, especially in the short term.

Can I transfer my existing ISA?

Yes. ISA transfers do not affect your annual allowance.

Is it better than a Cash ISA?

It depends on your goals. Cash offers stability, while investing offers growth potential.

Disclaimer

Capital at risk. Tax treatment depends on your individual circumstances and may change. This article is for information only and does not constitute financial advice. Variable rate correct as of 16/04/26. eToro account required. Your capital is at risk. ISA powered by Moneyfarm. ISA rules & promo Terms apply. UK residents only. The Cash ISA interest rate is variable and linked to the secure and protected Qualifying Money Market Fund (QMMF) your money is held in.