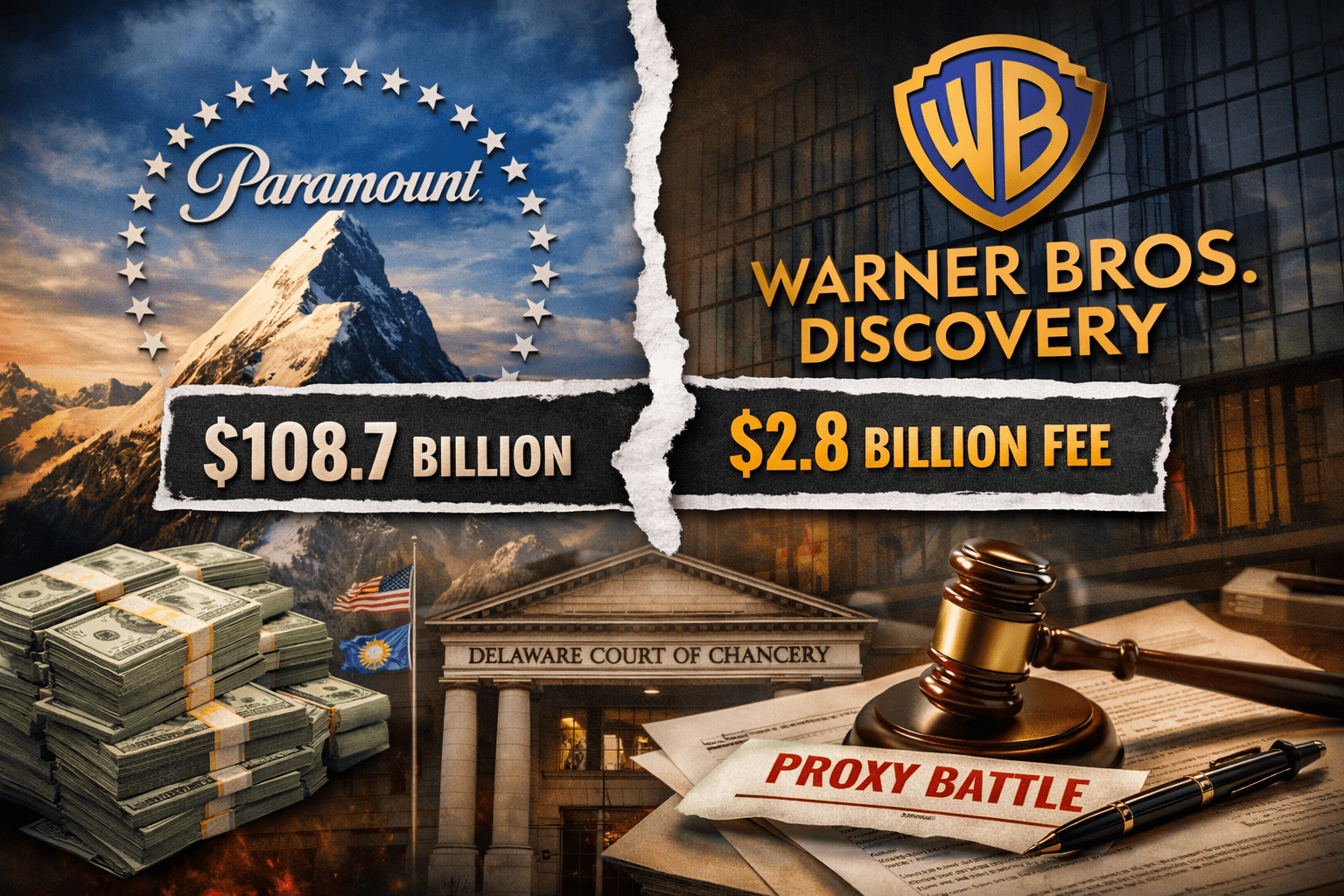

The Paramount–Warner Bros. Discovery takeover dispute is a live Delaware Court of Chancery contest as of January 12, 2026. Paramount Skydance (PSKY) has launched a $108.7 billion all‑cash hostile bid against WBD, which previously agreed to an $82.7 billion Netflix merger. The litigation focuses on SEC disclosure duties, a $2.8 billion termination fee, fiduciary obligations under Revlon, and a January 21, 2026 tender deadline that could trigger court‑mandated transparency.

Why this matters now: Litigation has formally placed WBD “in play,” and the tender clock runs toward January 21. Paramount is demanding disclosure of the financial analysis behind WBD’s choice to favor Netflix’s deal over the superior cash offer. Under Revlon duties and SEC proxy disclosure rules, this delayed transparency now carries material litigation and valuation risk.

This audit examines the $54 billion leverage stack supporting Paramount’s cash bid, the $2.8 billion Netflix termination fee, and SEC-mandated disclosure obligations related to WBD’s proposed cable asset spinoff, which plaintiffs describe as “virtually worthless.”

Paramount’s $108.7B Cash Bid: Leverage, Termination Fees, and Asset Risk

Asset impairment risk escalates as Paramount challenges the transparency of the Netflix‑Warner merger agreement. Disclosure has shifted from discretionary to mandatory. Investors require forensic clarity to assess whether fiduciary duties are being satisfied before the January 21 tender deadline expires. The absence of granular valuation data now constitutes a governance risk rather than a negotiating tactic.

Liquidity velocity remains constrained by the $2.8 billion termination fee owed to Netflix if the deal collapses. This fee creates immediate cash friction. Paramount must demonstrate that its $108.7 billion offer offsets approximately $4.7 billion in combined termination, transaction, and tax costs required to exit the Netflix agreement without impairing shareholder value.

Debt issuance exposure intensifies under Paramount’s proposed $54 billion leverage stack. Borrowing costs remain elevated in the 2026 rate environment. Larry Ellison’s $40 billion personal equity guarantee materially reduces execution risk, but senior debt covenants still require stress‑testing against post‑merger streaming cash flows and interest‑rate volatility.

Valuation multiples for legacy media assets increasingly depend on the terminal value of intellectual‑property libraries. The DC Comics universe and Harry Potter franchise anchor long‑duration cash flow assumptions. The proxy contest centers on whether WBD’s board is undervaluing Paramount’s $30‑per‑share cash offer to preserve strategic alignment with Netflix’s distribution ecosystem.

Statutory risk intensifies as Paramount seeks a bylaw amendment requiring shareholder approval for any cable‑asset spinoff. Such a transaction carries tax consequences and permanent revenue impairment. The maneuver targets the core financial architecture of the Netflix proposal by forcing a public referendum on the declining economics of linear television.

Acquisition risk increases when boards reject superior cash bids in favor of complex stock‑and‑distribution partnerships. Under Delaware Revlon doctrine, directors must prioritize value maximization once a sale becomes inevitable. Paramount’s filing argues that WBD’s directors may have subordinated liquidity certainty to strategic preference, exposing the board to judicial scrutiny.

Cash‑flow friction will persist throughout the January 21 tender window as institutional investors weigh certainty against optionality. In current M&A markets, cash carries a premium. Investors must determine whether a guaranteed $30 exit outweighs the uncertain upside of a Netflix‑aligned streaming entity burdened by termination friction and asset separation risk.

Synergy estimates supporting the Netflix merger remain unverified pending disclosure. Paramount’s lawsuit seeks access to internal financial models to test whether projected efficiencies justify rejecting a higher cash bid. Without this data, shareholders risk exchanging immediate liquidity for speculative future gains.

Interest‑rate exposure on the $54 billion debt component requires forensic review of Paramount’s hedging strategy. Variable‑rate exposure could compress interest‑coverage ratios rapidly. Credit deterioration would directly impair the long‑term stability of the combined studio entity.

Credit Architecture: The Ellison Guarantee and the $54B Leverage Stack

The Paramount proposal divides the $108.7 billion consideration between approximately $54.7 billion in equity and $54 billion in new debt. The transaction’s primary credit stabilizer is Larry Ellison’s $40 billion personal equity guarantee, an unprecedented commitment that establishes a liquidity floor rarely seen in hostile media acquisitions.

Despite this backstop, treasurers must model post‑transaction debt‑to‑EBITDA ratios under conservative revenue assumptions. Servicing a $54 billion issuance requires sustained free‑cash‑flow generation from library monetization. The durability of franchise revenues therefore becomes a credit variable, not a branding metric.

Paramount’s $30 per share cash offer exceeds Netflix’s implied $27.75 per share value, but the true advantage must account for deal-specific friction. After subtracting the $2.8 billion termination fee owed to Netflix and any tax liabilities from the proposed cable spinoff, the net value of Paramount’s bid remains materially higher. This demonstrates that, even after factoring in these costs, Paramount’s cash offer creates more immediate shareholder value and strengthens its position under Delaware fiduciary scrutiny.

Asset Impairment Risk: The “Virtually Worthless” Cable Spinoff

Paramount characterizes the proposed WBD cable spinoff as “virtually worthless,” directly challenging the valuation logic of the Netflix transaction. If assets such as CNN and legacy Discovery networks face structural decline, embedding them in a stock‑heavy deal may constitute an equity trap for shareholders.

The Netflix structure relies on isolating these assets to present a cleaner streaming‑centric balance sheet. Paramount’s proposed bylaw amendment blocks this maneuver by requiring shareholder consent. This forces WBD to confront the drag these assets impose on terminal value.

Friction Breakdown: Cost of Exiting the Netflix Agreement

| Expense Item | Paramount Cash Bid | Netflix Merger |

|---|---|---|

| Termination Fee | $0 | $2.8B |

| Transaction Friction | ~$1.2B | ~$4.7B |

| Shareholder Payout | $30.00 Cash | $27.75 Mixed |

| Regulatory Risk | Lower | Moderate |

For finance leaders, the Netflix deal presents a double‑jeopardy scenario. Equity underperformance combined with impaired cable assets could reduce realized value below $70 billion. Paramount’s litigation seeks to surface this downside before the tender deadline.

Proxy Governance and the Delaware Strategy

By filing in the Delaware Court of Chancery, Paramount invokes the strongest enforcement venue in U.S. corporate law. Revlon duties require directors to demonstrate value maximization once control changes become unavoidable. A $108.7 billion all‑cash offer raises the evidentiary bar for rejecting a lower bid.

The planned nomination of an alternative board signals escalation into a full proxy contest governed by SEC Schedule 14A disclosure rules. Institutional holders now face a governance decision rather than a strategic narrative.

The January 21 Tender Deadline

The January 21 expiration functions as a synthetic pressure mechanism. Failure to disclose Netflix deal analytics before this date increases the likelihood of court‑ordered disclosure or injunctive relief. Delay now increases transaction cost rather than preserving leverage.

The strategic irony is that resisting the Skydance bid may inflate the ultimate cost of the Netflix transaction. In 2026, M&A outcomes hinge not only on bid size but on the defensibility of rejection.

Boardroom FAQ: The Paramount-WBD Litigation

Why is Paramount suing Warner Bros Discovery for Netflix deal data?

Paramount (Skydance) argues that WBD’s board is hiding the financial analysis that justifies rejecting a higher $108.7 billion cash bid in favor of a lower $82.7 billion Netflix deal. They seek this data to convince shareholders to tender their shares before Jan 21.

What is the significance of the $2.8 billion termination fee?

WBD would owe Netflix $2.8 billion if it breaks their agreement to accept Paramount’s bid. This fee, plus other costs totaling $4.7 billion, represents a major liquidity hurdle that Paramount must prove its $30/share bid can absorb.

How does Larry Ellison’s $40 billion guarantee change the deal?

It provides "certainty of funds," a critical metric for regulators and shareholders. A personal guarantee of this size reduces the execution risk compared to a deal that relies on the volatile stock prices of the merger partners.

What is a Business Disruption Order in this context?

While not explicitly used yet, the Delaware court could issue an injunction that halts the Netflix merger process until WBD proves its fiduciary duty was met in rejecting the Paramount offer.

Why is the cable spinoff a central point of the lawsuit?

Paramount claims WBD is overvaluing the cable assets to make the Netflix deal look better. By requiring a shareholder vote on the spinoff, Paramount aims to prove that investors view the cable business as a liability, not an asset.

Will the Jan 21 deadline be extended?

Paramount has stated that any extension depends on the number of shares tendered. If institutional investors hold out for more data from the lawsuit, an extension is highly likely to keep the pressure on WBD.

Financial Insight:👉How Grok’s Regulatory Bans Turn AI Safety Into a 10% Revenue Risk👈

SEO Tags: #ParamountWBDTakeover #SkydanceProxyFight #NetflixTerminationFee #DelawareChanceryMandaA #MediaAssetValuation2026 #HostileTakeoverForensics #LarryEllisonEquityGuarantee