In today’s lending landscape, your FICO® Score can make the difference between securing a favorable personal loan and facing higher borrowing costs.

With the average U.S. FICO® Score standing at 715, even modest changes in your credit profile can significantly affect interest rates and loan accessibility. Personal loans, along with credit cards and other consumer credit tools, are not merely borrowing instruments—they are strategic financial tools that can help manage debt, build credit, and achieve life goals. Understanding the nuances of FICO scoring empowers borrowers to make informed choices and optimize their financial health.

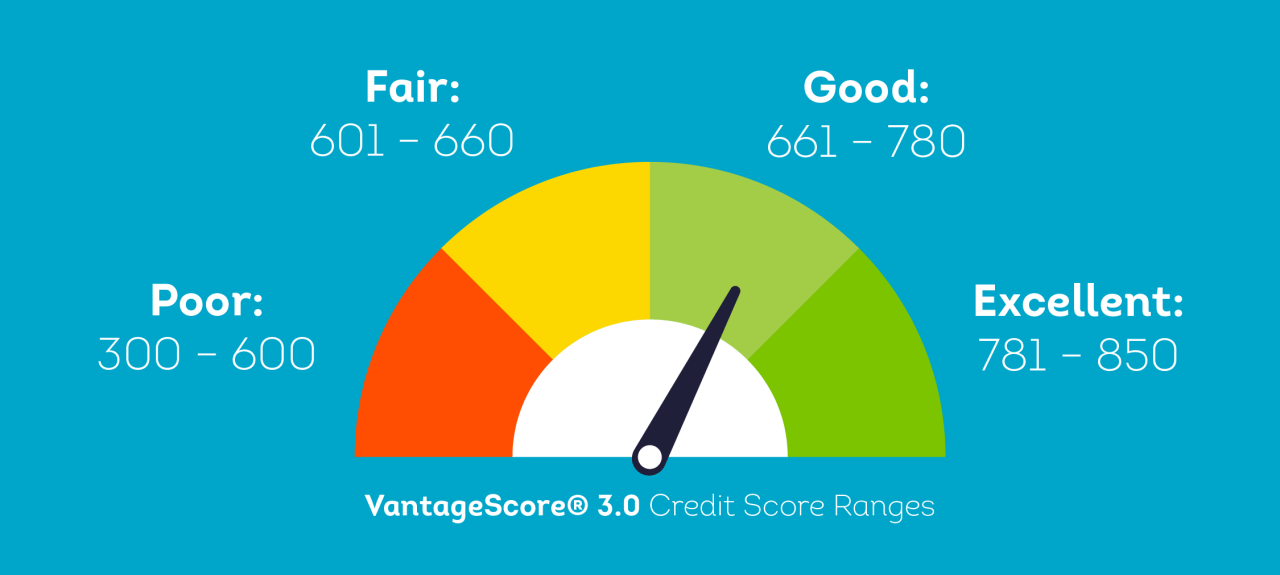

What a FICO Score Is and Why It Matters

A FICO® Score is a numerical representation of creditworthiness, ranging from 300 to 850, and is used by most lenders in the United States to evaluate risk. Higher scores indicate lower credit risk, which typically translates into lower interest rates, while lower scores signal higher risk, leading to costlier loans or potential denials. Scores above 670 are considered better than average, scores above 740 are excellent, and scores exceeding 800 are exceptional.

FICO scores are calculated based on five core factors: payment history, total debt owed, length of credit history, new credit activity, and the variety of credit types used. Each factor plays a critical role in determining how lenders perceive your reliability.

Multiple versions of FICO scores exist, with slightly different weighting methods. The most widely used version remains FICO Score 8, although versions 9 and 10 Suite are increasingly applied. Notably, modern scoring models are more forgiving of isolated late payments and consider credit utilization trends over time, which helps borrowers with minor past mistakes maintain favorable scores.

How Your FICO Score Influences Personal Loan Interest Rates

Your FICO score directly affects the interest rate a lender offers on a personal loan. Borrowers with excellent credit are rewarded with the lowest rates, while those with fair or poor credit face higher costs. As of September 2025, Credible reports that the average personal loan interest rates illustrate this impact: individuals with excellent scores between 720 and 850 can secure rates around 10.72% for three-year loans and 16.34% for five-year loans.

Borrowers in the very good range of 690–719 may see rates of 13.49% on three-year loans and 19.23% on five-year loans. Those with scores between 660–689 face rates of 20.28% for three-year loans and 24.43% for five-year loans, while scores in the 620–659 range may lead to 29.25% and 31.44% respectively. Borrowers with scores below 620 can expect APRs from 32% to 36%, highlighting how even small improvements in credit can yield substantial savings.

Why Lenders Rely on Your FICO Score

Lenders use FICO scores to quantify risk and predict the likelihood of timely repayment. A strong score indicates a history of responsible borrowing and demonstrates reliability, which encourages lenders to offer lower interest rates. Conversely, a lower score signals higher risk, which can result in higher costs or denial of credit. While lenders also consider income, employment history, and other financial factors, your FICO score remains a primary determinant of both approval and the cost of borrowing.

This FICO chart breaks down credit score categories from Poor to Excellent, helping borrowers understand how their score affects loan eligibility and interest rates.

Improving Your FICO Score to Reduce Interest Rates

Even modest improvements in your credit profile can lead to lower rates. Timely payments remain the most critical factor, reflecting positively on your payment history, which constitutes the largest portion of the score. Keeping credit utilization below 30%, maintaining a healthy mix of installment loans, credit cards, and retail accounts, and avoiding frequent credit applications all support score growth.

Regularly reviewing your credit report to correct errors ensures that your score accurately reflects responsible financial behavior. The combination of consistent payment history and responsible credit use can gradually enhance your FICO score, opening access to better loan terms.

Additional Factors Affecting Loan Rates

Interest rates are also influenced by the loan amount and repayment term. Short-term loans generally carry lower interest rates but require higher monthly payments, while longer-term loans reduce monthly obligations but increase overall interest costs. Similarly, lenders may perceive smaller loan amounts as higher risk if administrative costs outweigh potential profit, which can result in slightly higher rates. Borrowers must carefully balance their financial goals with the cost of borrowing to determine the most advantageous loan structure.

People Also Ask About FICO

Here are some common questions borrowers have about FICO scores and personal loan interest rates, with clear answers to help guide your financial decisions.

How can I qualify for the best personal loan rates?

Borrowers can qualify for the lowest rates by maintaining a FICO score above 720, keeping debt levels manageable, paying bills on time, and limiting new credit inquiries. Comparing multiple lenders also helps identify the most competitive rates.

What is considered a good FICO score for a personal loan?

A score of 690 or above is generally considered good, while scores above 740 are excellent and often qualify for the lowest interest rates.

Can I get a personal loan with a low credit score?

Yes, but expect higher interest rates. Options like secured loans, co-signed loans, or credit-builder loans may provide alternative avenues for borrowing.

How long does it take to improve a FICO score?

Improvement can take several months to a year, depending on current debts, payment history, and credit management habits. Consistency in paying bills on time and lowering credit utilization has the most immediate effect.

Are there alternatives to personal loans for those with low credit scores?

Alternatives include secured loans, credit-builder loans, or borrowing with a co-signer. Each option has its own terms and risks, so it’s important to carefully assess each before proceeding.

Conclusion: The Critical Role of FICO in Personal Loan Success

Your FICO® Score is central to your ability to secure affordable personal loans and manage student loan repayments effectively. By understanding how scores are calculated, maintaining responsible credit habits, and monitoring your credit profile, you can significantly improve the interest rates available to you.

Even small improvements in your FICO score can lead to meaningful savings over the life of a loan and may also impact the terms of student loan refinancing or consolidation, demonstrating that strategic credit management is not just beneficial—it is essential for financial stability. Whether seeking to consolidate debt, finance a major purchase, or establish a stronger credit history, managing your FICO score effectively is a cornerstone of smart personal finance.