A Home Equity Line of Credit (HELOC) can give homeowners flexible access to their home’s equity, but it comes with both opportunities and risks.

A Home Equity Line of Credit (HELOC) offers a revolving line of credit secured by your home’s equity, allowing you to borrow as needed and pay interest only on the funds you use.

For many homeowners, this flexibility can be more advantageous than a personal loan or home equity loan. As of early 2025, the average HELOC credit limit was over $149,000, while most borrowers used just over $45,000 on average according to Experian. However, understanding both the advantages and potential drawbacks is critical before committing to a HELOC.

Factors to Consider Before Applying for a HELOC

Before applying, evaluate your financial situation carefully. Lenders typically allow you to borrow up to 85% of your home’s appraised value minus any outstanding mortgage balance. Your creditworthiness also affects your interest rate; a higher credit score generally means lower rates. Finally, ensure your income and budget can accommodate potential monthly payments, especially since HELOCs have variable rates that can rise over time.

Pros of a HELOC

HELOCs offer several benefits for disciplined borrowers.

Lower interest rates: HELOC interest rates are generally lower than those of personal loans or credit cards. “Home equity rates are lower than the double-digit rates you’ll find on personal loans or credit cards, which can make a big difference when consolidating debt or funding home renovations,” says Linda Bell, home lending expert at Bankrate.

Flexible terms: With a HELOC, you borrow only what you need, when you need it, and make payments on the borrowed amount. Many lenders allow interest-only payments during the draw period, typically 10 years, which helps manage monthly obligations. Some HELOCs even allow partial conversion of the balance to a fixed rate, protecting against future interest spikes.

Tax advantages: If HELOC funds are used for substantial home improvements, interest may be deductible under IRS rules, potentially saving homeowners money compared to other credit options.

Potential credit benefits: Timely HELOC payments can improve your FICO score over time by demonstrating responsible use of credit, although a temporary dip can occur from the hard credit inquiry and the new account affecting average account age.

High borrowing limits: HELOCs are designed for substantial borrowing. While the minimum line may be $10,000, some lenders offer credit lines as high as $750,000 or even $1 million, depending on your home’s equity and combined loan-to-value ratio (ICE Mortgage Technology & Experian).

Cons of a HELOC

Despite their advantages, HELOCs carry significant risks.

Variable interest rates: Unlike home equity loans, HELOCs have variable rates tied to market conditions. Your payments can increase sharply if rates rise, creating a potential financial strain.

Your home is collateral: Since a HELOC is secured by your home, failing to make payments could result in foreclosure. Reduced equity also limits your financial flexibility if property values drop.

Potential to overborrow: Interest-only payments during the draw period can create a false sense of available funds. If you do not manage repayments carefully, the transition to principal-and-interest payments can dramatically increase monthly obligations.

Additional fees: While HELOCs often have lower closing costs than home equity loans, borrowers may face origination fees, annual fees, early cancellation penalties, or inactivity fees. Comparing lenders and negotiating fees is essential to avoid unexpected costs.

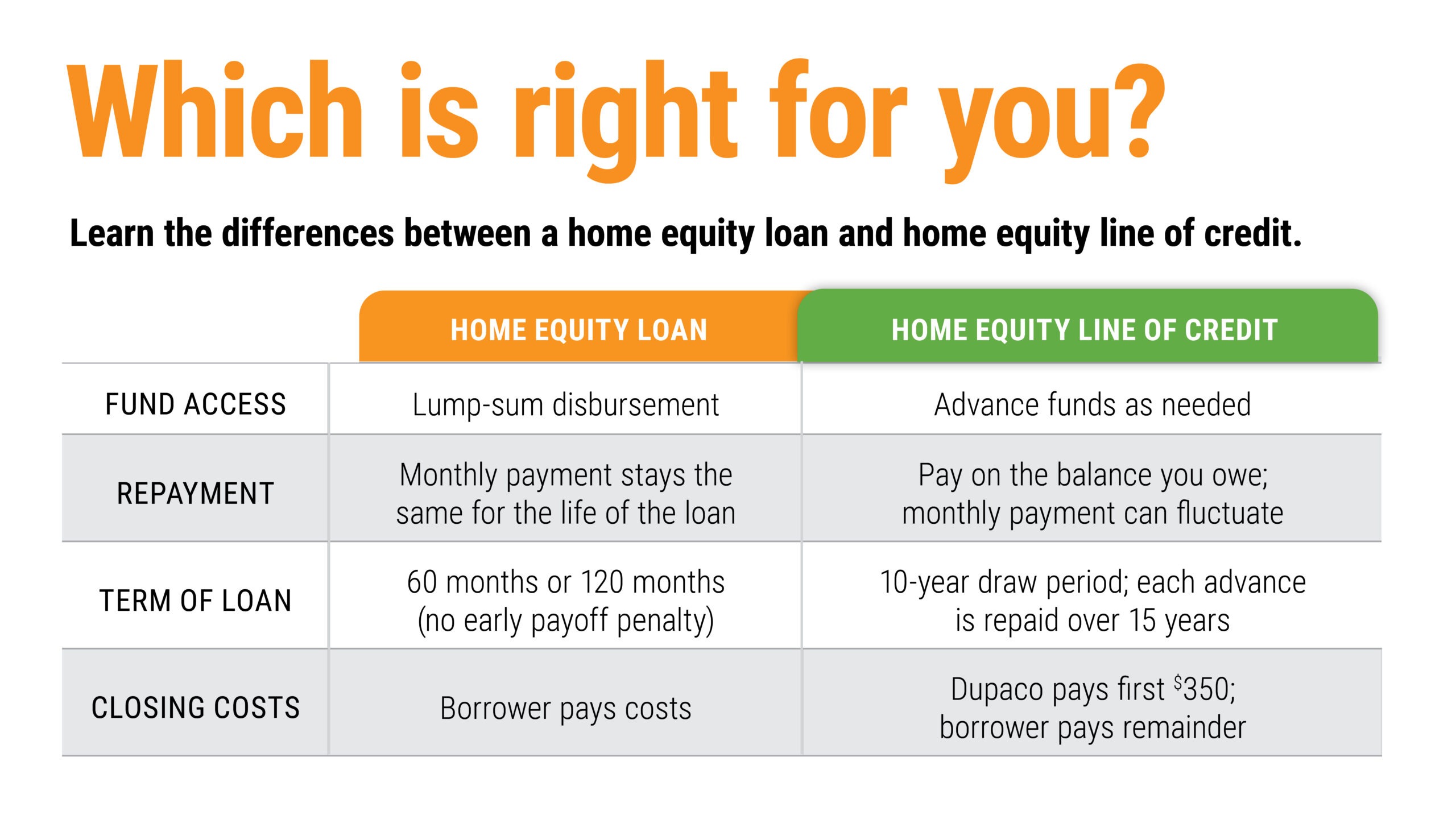

Dupaco's table Comparing Home Equity Loans and HELOCs to determine the best borrowing option for your financial needs.

Alternatives to a HELOC

If a HELOC isn’t suitable, consider other borrowing options:

Home equity loan: Provides a fixed lump sum with a fixed rate. Good if you know exactly how much you need upfront.

Cash-out refinance: Replaces your mortgage with a larger loan, giving you ready cash based on home equity. Best if you can secure a lower interest rate and plan to stay in your home long-term.

Personal loan: Unsecured with a fixed rate and monthly payment, but typically higher interest rates and lower borrowing limits than a HELOC. Unlike a HELOC, your home is not at risk.

People Also Ask

What is the difference between a HELOC and a home equity loan?

A HELOC is a revolving line of credit with a variable interest rate, whereas a home equity loan provides a lump sum with a fixed rate.

Can I use a HELOC for anything?

Yes, HELOCs can be used for home improvements, debt consolidation, education, or emergencies, but using them for investments that increase home value or financial stability is advisable.

Are HELOC interest payments tax-deductible?

Interest may be deductible if used for substantial home improvements. Consult a tax professional for specific guidance.

How does a HELOC affect my credit score?

Opening a HELOC involves a hard-credit check, which may cause a temporary dip in your FICO score, but on-time payments can help improve your credit over time (Experian).

Is a HELOC better than a personal loan?

A HELOC generally offers lower interest rates and flexible borrowing compared to a personal loan, but the risk is higher because your home secures the loan.

Conclusion

Home Equity Lines of Credit offer significant flexibility, high borrowing limits, and potential tax advantages, making them a useful tool for disciplined homeowners. However, variable interest rates, the use of your home as collateral, and potential fees highlight the importance of careful planning.

When considering a HELOC, evaluate your financial habits, intended use of funds, and ability to manage variable payments. For homeowners needing flexible access to substantial cash over time, a HELOC can be a powerful financial instrument—but only if used wisely.